The statement of capital provides a snapshot of a company’s share capital at a certain date. As at that date, it will show:

- the different share classes that exist;

- the amounts invested; and

- the rights attached to shares issued.

The statement of capital does not show who owns the shares, which is instead shown in a company’s register of shareholders. Sometimes, however, a list of shareholders must be submitted to Companies House alongside the statement of capital.

A company will maintain its own statement of capital, often using software such as Inform Direct. When it’s submitted to Companies House as part of a submission, anyone can view the statement of capital for a company on the public register.

Manage company shares the easy way

Inform Direct is the easy way for companies to manage company shares.

> Straightforward step by step processes

> Companies House forms produced

> Print compliant resolutions and board minutes

> Register of shareholders updated automatically

> Easy to file the next confirmation statement

What types of companies need a statement of capital?

All companies with share capital need to maintain a statement of capital. That includes:

- Private companies limited by shares (the vast majority of UK companies)

- Public limited companies

- Community interest companies (CICs) set up as a private companies limited by shares or public limited companies

- Unlimited companies with share capital

These companies need a statement of capital, even if they are dormant.

Types of business that don’t need a statement of capital include:

- Companies limited by guarantee (and community interest companies set up as guarantee companies)

- Unlimited companies without share capital

- Limited liability partnerships (LLPs)

- Limited partnerships

What’s the law governing the statement of capital?

The statement of capital was introduced on 1 October 2009 as part of the changes implemented by the Companies Act 2006. It replaced the previous regime, in which there was an upper limit to the number of shares (‘authorised share capital’) which could be issued.

For new companies formed with the model articles from 1 October 2009 (and other companies that amend their articles of association accordingly), the number of shares in issue can be increased without having to re-negotiate an arbitrary ceiling. Instead, companies limited by shares must maintain and in certain circumstances submit to Companies House the statement of capital.

The Companies Act 2006, as since amended by the Small Business, Enterprise and Employment Act 2015, details the contents of the statement of capital.

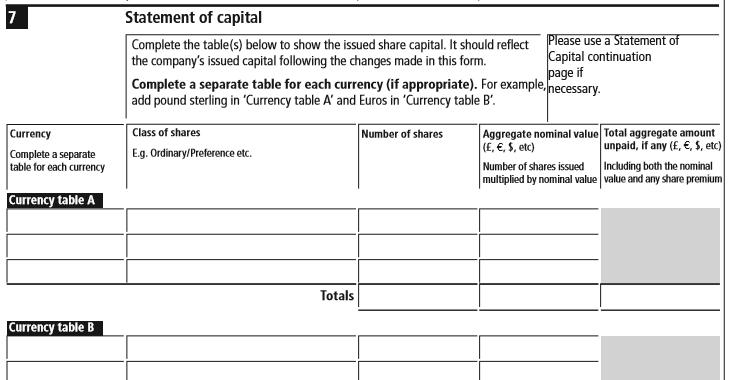

Part of the statement of capital, as featured in the SH02 paper form

What must be included in the statement of capital?

A valid statement of capital must include:

- The total number of shares in the company

- The aggregate nominal value of the company’s shares – calculated by multiplying the number of shares in issue by the nominal value of each share. If multiple share classes exist, this calculation should be undertaken for each class. The figures are then added together.

Example 1

ABCD Limited has two classes of shares, Ordinary £1 and Preference £0.10 shares.

There are 100 of the Ordinary shares in issue, so the aggregate nominal value of this class is 100 x £1 = £100.

There are 10 of the Preference shares in issue, giving a total nominal value for the class of 10 x £0.10 = £1.

The aggregate nominal value to be reported in the statement of capital is therefore £101.

- The total amount unpaid on the company’s shares – Shares might be issued to a shareholder without them paying for them at the time of issue. In this case, they are unpaid shares. It’s also possible to have partly paid shares, where part but not all of the amount due is paid. In both cases, the company might choose to call unpaid amounts at a later date. The total amount unpaid is simply the sum of all unpaid amounts on all shares in issue.

Example 2

EFGH Limited has one class of Ordinary shares with a nominal value of £1.

100 shares have been issued unpaid. Ultimately, the shareholders have agreed to pay £3 per share: this comprises the £1 nominal amount and £2 share premium per share.

The total amount unpaid to be reported includes both unpaid nominal amounts and unpaid share premium. So the total amount unpaid for EFGH will be 100 x £3 = £300.

Example 3

IJKL Limited has two classes of share, with 100 Ordinary £1 and 5 Preference £10.00 shares issued.

The 100 Ordinary shares have been issued unpaid with the £1 nominal amount remaining unpaid. There is therefore a total of 100 x £1 = £100 unpaid on this share class.

The Preference shares are currently partly paid, with £7 of the £10 still to pay. The amount unpaid on this share class is therefore 5 x £7 = £35.

IJKL will have to report a total amount unpaid of £100 + £35 = £135.

While IJKL has different amounts unpaid on different share classes, it would also be possible to have different amounts unpaid in a single share class. That could mean shareholders owe different amounts, which might be the case if a number of share issues have taken place. The calculation, however, will work in much the same way.

Example 4

MNOP Limited has 3 classes of share and there have been a number of share issues within the different classes. However, all the shares are fully paid with no unpaid amounts remaining.

MNOP can therefore include a total amount unpaid of £0 in its statement of capital.

Most companies will be in the position of reporting a total amount unpaid of £0.

For each class of share, a statement of capital must include:

- The name of the share class – This is a basic reference to identify the share class. It is required even if there’s only one class in existence. Popular examples include Ordinary, Ordinary A, Preference etc., often giving a strong clue to the type of shares they are.

- Prescribed particulars of the rights attached to shares in the class – the prescribed particulars are the rights, obligations and other conditions that pertain to shares in this class. They include details such as voting rights, dividend rights and any right to redeem the shares. While these details might also be documented in the company’s articles of association, they must be documented here. It’s not permitted simply to refer to another document, such as the articles.

- The total number of shares in that share class

- The currency in which the shares are denominated – while most share classes are denominated in Great British Pounds (‘GBP’), Euro, Yen and US Dollar shares are also fairly common. There’s a whole range of other currencies recognised by Companies House. These may, for example, be appropriate for a class of shares if the bulk of the company’s trading activities will take place in the respective country where that currency is used.

- The aggregate nominal value of shares of that class – calculated by multiplying the number of shares in issue for the class by the nominal value of each share.

There’s no need to show the amount paid up and unpaid on each share. The only requirement is to state the aggregate amount unpaid on the company’s shares. In the past, shares had to be separated out in the statement of capital by combinations of amounts paid and unpaid per share, which was often a real chore for companies with a complex history of share issues or reorganisations.

The change to the structure of the statement of capital doesn’t remove the need for a company to maintain accurate records of the unpaid amounts due on different shares. A comprehensive shareholder management tool like Inform Direct is invaluable here. If the company later wants to call an unpaid amount, it will need to have accurate and up to date information on which shares it applies to, the amount that’s unpaid and which shareholders hold the shares where the call is due.

When is the statement of capital needed?

Although the Companies Act defines it as a separate statement, often the statement of capital is included within a number of other Companies House forms. That’s true whether the form is submitted on paper or electronically. Either way, a service like Inform Direct will automatically assemble a compliant statement of capital that can be submitted.

Firstly, a statement of capital is required by companies limited by shares when first forming the company via form IN01. This gives an illustration of the company’s initial share capital.

The annual confirmation statement (submitted on form CS01) can include a statement of capital as part of the form. It can be included each year if the company chooses to submit it, but the statement of capital only needs to be included where the share capital position has changed since the last statement of capital submitted. That might, for example, occur when in the course of a confirmation period a company has made a call on shares that were previously unpaid or partly paid.

It should now be very rare indeed that a company still needs to submit an annual return (on form AR01), but any such filing will need to include a statement of capital.

An updated statement of capital also needs to be completed and submitted to Companies House when various changes to a company’s share capital are made. The following forms are examples of cases where the statement of capital is either included within the form itself or needs to be submitted alongside the form:

- SH01 – Return of allotment of shares

- SH02 – Notice of consolidation, sub-division, redemption of shares or re-conversion of stock into shares

- SH05 – Notice of cancellation of treasury shares

- SH06 – Notice of cancellation of shares

- SH07 – Notice of cancellation of shares held by or for a public company

- SH14 – Notice of redenomination of shares

- SH15 – Notice of reduction of capital following redenomination

- SH19 – Statement of capital when reducing capital in a company

If a shareholder asks for this information, a company should also be prepared to send them the current statement of capital.

Where can I find a company’s latest statement of capital?

A company will often maintain its own up to date summary of the statement of capital.

The last update provided to Companies House can be viewed by searching the company filing history. Although many companies will regularly submit capital changes when the structure of shares in the company is changed, for others updates will be far less frequent. As it’s not compulsory to submit a statement of capital as part of the confirmation statement, for companies which have not changed their share capital the last statement could be as far back as:

- Incorporation (on the IN01 form); or

- The first confirmation statement filed from 30 June 2016 (for companies formed before that date)

Inform Direct is the innovative and easy way to manage a company's shares, make new share allotments, record share transfers, process share reorganisations and more.

A previous version of this article was published on 27 May 2016.