Most companies only ever have one type of share (or class of share). These are commonly called ordinary shares and will be the ones the company was incorporated with. The typical rights that go with ordinary shares are:

- Each share is entitled to one vote in any circumstances

- Each share has equal rights to dividends

- Each share is entitled to participate in a distribution arising from a winding up of the company.

These are the rights conferred by the Model Articles of Association for private limited companies.

However, some companies choose to have two or more different types of share, sometimes referred to as ‘alphabet shares’. It’s relatively straightforward to create a new share class. Indeed, if the shareholders consent then a company can have as many different share classes as it likes, each representing a different type of share.

It is the articles of association which set out the division of shares into their different classes. The rights attached to these classes are called the prescribed particulars and are included in the statement of capital.

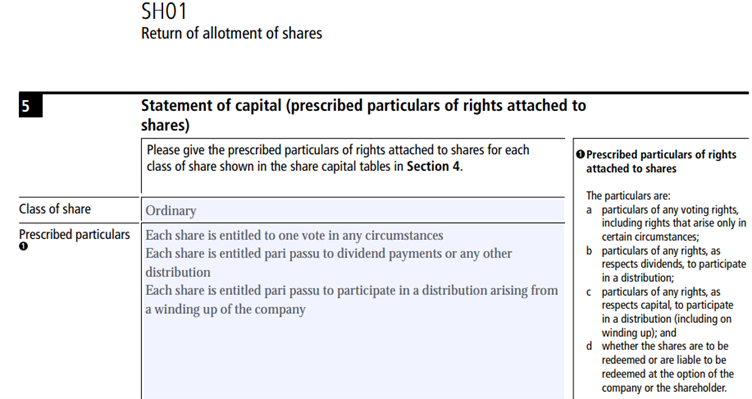

An example of prescribed particulars that define the rights attached to shares on a SH01 form, used for allotting new shares. Pari passu means ‘on an equal footing’.

Equally, the shareholders’ rights for different classes of shares do not have to be different. In fact, different share classes can have identical rights to other classes. In some companies, ‘alphabet shares’ (ordinary A Shares, ordinary B Shares, etc) with identical rights are issued to different shareholders.

Creating different share classes in this way might allow dividends to be paid to some shareholders but not to others. The company should be careful to ensure that any such strategy does not constitute a breach of HMRC rules and guidelines.

Manage your company's share classes the easy way

Inform Direct makes it easy to manage share classes, letting you record new share classes and changes to existing class rights.

Start nowIf a company has more than one type of share the main differences between them will be found in one or more of the following areas:

1. Entitlement to dividends

The right to receive dividends can vary from one type of share to another. Shares may have the right to:

- normal dividends

- preferential dividends (that is, the right to be paid a dividend before other share classes or at a certain fixed level)

- a dividend only in certain circumstances

- no dividends at all.

Tax is an important consideration with dividends, particularly when directors are deciding the right mix of salary and dividends to pay themselves out of the company. For details of how dividends are taxed, please see our article on dividend taxation and another dedicated to dividends and higher rate taxpayers.

2. Entitlement to capital on winding up

If the company is dissolved, any assets left after the company’s debts are paid can be distributed to shareholders. However, different share classes may have different rights to capital distribution – with some shares ranking first and others only paid if sufficient assets remain after others have received their full distribution of capital.

3. Voting rights

Usually, this is as simple as shares either carrying voting rights or not. However, weighted or tiered voting rights are also possible – so, for example, shares may carry extra voting rights in certain circumstances or on certain important matters affecting the company.

While there are a few conventions which are best followed to avoid any misunderstandings, a company can call shares by whatever name it likes. That said, you cannot assume that shares called ordinary in one company will have exactly the same rights as the ordinary shares in another company. The surest way to ascertain what rights go with a particular share class is to read the most recent statement of capital of that company, which will contain the prescribed particulars of the shares.

The reasons for a company wanting to have different share classes will generally fall into one of these categories:

- To attract investment by offering different shareholder rights to investors

- To push dividend income in a certain direction

- To remove (or enhance) voting powers of certain individuals

- To motivate staff (to remain as employees)

Provided it follows due process, and subject to any restrictions in its articles of association, a company can create a new share class at any time. When it needs a new share class a company can choose to either create a new one or convert an existing share class into one or more new ones.

Most classes of share will fall into one of the following categories:

1 Ordinary shares

These carry no special rights or restrictions. They rank after preference shares as regards dividends and return of capital in the event of the company being wound up. But they carry voting rights (usually one vote per share) not normally given to holders of preference shares.

Some companies create more than one class of ordinary shares – e.g. “A ordinary shares”, “B ordinary shares” etc. This gives flexibility for different dividends to be paid to different shareholders or, for example, for pre-emption rights to apply to some shares but not others.

In some cases, different classes of ordinary share may be of different nominal values. For example, there may be £1 ordinary shares and £0.01 ordinary shares. If each share had the right to one vote (and assuming the shares were issued at their nominal value), then the £0.01 ordinary shareholders would get 100 votes per £1 paid while the £1 ordinary shareholders would get 1 vote per £1 paid.

2 Deferred ordinary shares

A company can issue shares which will not pay a dividend until all other classes of shares have received a minimum dividend. Thereafter they will usually be fully participating. On a winding up they will only receive something once every other entitlement has been met.

Deferred shares are generally issued to founders and directors of a company and/or investors. They represent a long-term investment that is locked away until a major liquidity event occurs such as dissolution or acquisition. They may have conditions attached regarding the company’s performance and share price, or they may reach term (‘vest’) only after a specified number of years.

Deferred shares are used to incentivise long-term commitment to the company from employees, executives and investors, since they are slow to mature but can grow significantly over time of the company performs well.

3 Non-voting ordinary shares

Voting rights on ordinary shares may be restricted in some way – e.g. they only carry voting rights if certain conditions are met. Alternatively, they may carry no voting rights at all. They may also preclude the shareholder even attending a General Meeting. In all other respects they will have the same rights as ordinary shares.

Non-voting ordinary shares are usually issued to employees and to family members of the main stakeholders in the company. They confer benefits such as dividends, but don’t allow involvement in the running of the company by voting at meetings.

4 Redeemable shares

The terms of redeemable shares give the company the option to buy them back in the future; occasionally, the shareholder may (also) have the option to sell them back to the company, although that’s much less common.

The option may arise at or after a specific date, between two dates or be effective at any time the shares are in issue. The redemption price is usually the same as the issue price but can be set differently. A company can only redeem shares out of profits or the proceeds of a new share issue, which may restrict its ability to redeem shares even if the directors would like to exercise the option.

If a company chooses to have redeemable shares, it must also have non-redeemable shares in issue. At no point can all of its share capital be made up of redeemable shares.

Redeemable shares give investors a degree of liquidity in that they can offer the ability to sell back their shares at a predetermined price in the future. This can make investing more attractive by providing investors with an exit strategy. Redeemable shares can also be useful for managing capital structure by adjusting the number of shares in issue in response to changing market conditions.

For further uses of redeemable shares with examples, please see our dedicated article on redeemable shares.

5 Preference shares

These shares are called preference or preferred since they have a right to receive a fixed amount of dividend every year. This is received ahead of ordinary shareholders. The amount of the dividend is usually expressed as a percentage of the nominal value. So, a 5% preference share priced at £1 will pay an annual dividend of 5p. The full entitlement will be paid every year unless the distributable reserves are insufficient to pay all or even some of it.

On a winding up, the holders of preference shares are usually entitled to any arrears of dividends and their capital ahead of ordinary shareholders. Preference shares are usually non-voting (or only have a vote only when their dividend is in arrears). They are attractive to investors and useful for raising capital without giving away control of the company.

For more detail please see our article about preference shares.

… there’s nothing to stop a shareholder holding more than one class of share in the same company and thereby benefiting from the differing rights (e.g. voting or dividend entitlement) that each class offers.

6 Cumulative preference shares

If the dividend is missed or not paid in full then the shortfall will be made good when the company next has sufficient distributable reserves. It follows that ordinary shareholders will not receive any dividends until all the arrears on cumulative preference shares have been paid.

By default, preference shares are cumulative but many companies also issue non-cumulative preference shares.

7 Redeemable preference shares

Redeemable preference shares combine the features of preference shares and redeemable shares. The shareholder therefore benefits from the preferential right to dividends (which may be cumulative or non-cumulative) while the company retains the ability to redeem the shares on pre-agreed terms in the future.

Most companies start by just having one type of shares in the form of an ordinary share class. These will typically carry equal rights to voting, capital and dividends. The issue of new shares after company incorporation will generally be allotments of these ordinary shares, unless circumstances suggest a need for flexibility or varied rights.

Just as a company may issue shares in multiple share classes, there’s nothing to stop a shareholder holding more than one class of share in the same company and thereby benefiting from the differing rights (e.g. voting or dividend entitlement) that each class offers.

Inform Direct is the innovative and easy way to record new share classes, make changes to existing share classes and process share class conversions.

A previous version of this article was published on 16 March 2015. The latest update was on 18 April 2023.

‘Very useful piece of information. Simple and clear’ – English-Polish Interpreter

Thanks a lot for the information. Very useful.

Its was very helpful thank you