A company can have different types of shares depending on its capital requirements. All companies will have a type of ordinary share, which are non-redeemable (sometimes referred to as irredeemable) shares with full voting rights. Companies may then have other types of ordinary share, preference shares which give a preference to the holders – usually in respect of dividends and capital, redeemable shares and other share types. The preference and other share types can be irredeemable or redeemable shares.

Only redeemable shares can be redeemed. If a company wants to buy back non-redeemable shares then it will need to purchase its own shares or complete a share capital reduction.

A company cannot only have redeemable shares and must have at least one non-redeemable share in issue. The company, therefore, must have one or more non-redeemable ordinary shares.

What are redeemable shares?

Redeemable shares are shares that a company has agreed it will, or may, redeem (in other words buy back) at some future date. The shareholder will still have the right to sell or transfer the shares subject to the articles of association or any shareholders’ agreement. Redeemable shares will often be a type of preference share that provide for some form of preferential rights over ordinary shares. This preference may be payment of dividends, return of capital or in some instances voting rights. However, redeemable shares do not have to be preference shares.

The redemption terms will have been set out in the share issue documents, the prescribed particulars for the shares and, potentially, included in the company’s articles of association. The redemption terms will include the redemption date or dates and the basis for the redemption price.

The redemption date may be:

- a fixed date (eg redeemed on a set date or a set number of years after issue);

- at the directors’ discretion;

- at the company’s option; or

- at the shareholder’s option.

The redemption price will generally be a fixed amount or calculated in a fixed way. This can be the same as the nominal value, the issue price or any other price.

Why issue redeemable shares?

Companies will issue redeemable shares for a variety of reasons. The main two are:

1. To provide a third party investor (eg a venture capitalist) with an agreed exit strategy albeit subject to the company having sufficient distributable reserves.

Using redeemable shares as an exit strategy

An investor agrees to put in £100,000 on the basis of receiving a minimum of £500,000 back after five years. To provide an element of assurance the company issues 1,000 redeemable A preference £1 shares at £100 each with these shares having the right to a cumulative annual dividend of £50 for five years and then being redeemable by the company at the end of the fifth year after the date of issue at £250 per share. There is no guarantee that shares will be redeemed on the redemption date or if the full redemption price will be paid if the company does not have enough distributable profits or assets to make the payments.

The redeemable shares until redeemed could still have the same voting rights as the ordinary £1 shares already in existence.

2. To provide a method for the company to buy out certain shareholders.

Using redeemable shares to buy out a shareholder

The directors of a company have issued 50 convertible redeemable shares to each of the company’s five employees, which convert to ordinary shares after five years but at any time before then the company has the right to redeem the shares at par. Two years after the shares where issued an employee leaves employment and the directors do not want the former employee to hold shares in the company. They, therefore, use the company’s option to redeem these shares at par and the former employee is no longer a shareholder.

What to consider before issuing redeemable shares

A company, before issuing the shares, should ensure that its articles of association allow redeemable shares to be issued. If not, then the company can either amend its articles of association or pass an ordinary resolution giving authority to the directors to issue redeemable shares.

Provided that the directors have the right to issue redeemable shares they need to agree the terms and conditions of the redeemable shares and include these in the share issue documents, the prescribed particulars for the shares and, if considered appropriate, in the company’s articles of association.

Once the above has been completed the redeemable shares can be issued. We look in more detail at how to issue shares in another article.

What needs to be done to complete a redemption of shares

The procedures to follow to redeem shares will depend on a number of factors including:

- the company’s articles of association;

- the prescribed particulars of the shares;

- how the redemption is to be financed;

- any shareholders’ agreement; and

- whether or not the company is following the terms of the redemption set out in the issue documents or the articles of association.

Where the shares are redeemed in line with the articles of association then, unless required by them, the shareholders do not need to approve the redemption. The directors then, provided the company has sufficient distributable reserves or is issuing new shares with sufficient proceeds, just need to pass a board resolution approving the redemption.

If, however, the articles of association or any shareholders’ agreement require the redemption to be approved by the shareholders then the appropriate ordinary or special resolution, as applicable, of the shareholders will be required in addition to a board resolution.

Where the redeemable shares are being purchased other than in accordance with the articles of association then the buyback of the shares should be treated as a purchase of own shares and the requirements for doing this followed.

There are certain statutory restrictions on the redemption of shares. The main requirement, as for a purchase of own shares, is that the company may only redeem the shares out of distributable reserves (basically accumulated profits) or the proceeds of a new issue of shares. However, if the company is a private limited company then it can potentially finance the redemption in part or in full out of capital. All available distributable reserves and the proceeds of any new share issue must be used first. This is called a permissible capital payment and the additional requirements, including shareholder approval, are explained in our Using capital for a redemption or purchase of own shares article.

As for a buyback of shares, the shares being redeemed must be fully paid.

In addition once the company has redeemed the shares these shares must be cancelled.

Recording and reporting requirements

Once the share redemption has been made the company should:

- Retain a copy of the resolution of the directors and any resolution of the shareholders approving the redemption.

- Enter the necessary transactions in the company’s accounting records, including:

- payment for the redemption;

- reduce the issued capital by the nominal value of the shares redeemed;

- reduce the share premium account by the lower of any premium initially received on issue of the shares redeemed and the current value of the share premium account; and

- transfer from the profit and loss account to a capital redemption reserve the amount of the redemption paid out of distributable reserves.

- For a private limited company where the redemption is partly or wholly financed out of capital then retain copies, as applicable, of the following:

- directors’ statement of solvency;

- special resolution approving the share redemption;

- any necessary auditors’ report;

- notice published in the London Gazette; and either

- notice published in a national newspaper; or

- record of notification to all creditors.

- Where the redemption was approved by the shareholders file a copy of the shareholders’ resolution at Companies House.

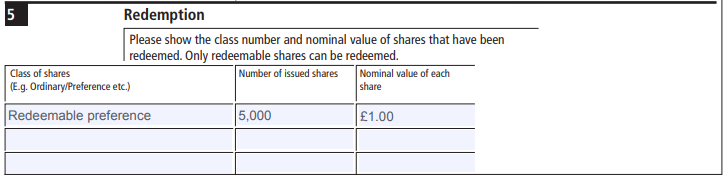

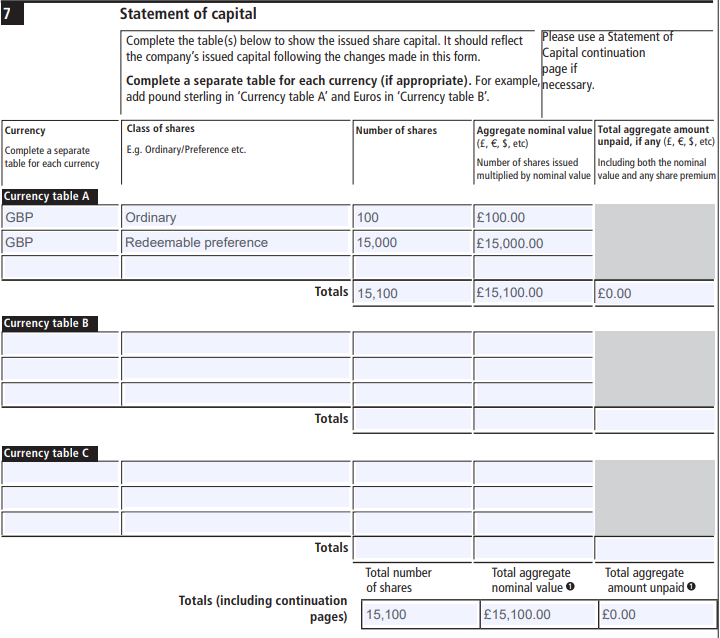

- In all cases complete and file form SH02 at Companies House. Currently this needs to either be a paper copy or an electronic copy of the form sent to Companies House using their document upload process. Sections 1,2,5,7 and 8 should be completed and then section 9 signed for the company.

These examples of sections 5 and 7 show where a company has redeemed 5,000 of its existing 20,000 redeemable preference shares.

- Update the register of shareholders and other company records for the number of shares redeemed and hence cancelled by the company for each shareholder.

- Issue new share certificates if necessary.

Tax and share redemptions

The price paid on redemption can have taxation implications on the seller of the shares. In particular, any amount over the initial issue price paid to the company will normally need to be treated as a distribution. This amount will be treated as taxable income and not as a capital gain, unless certain requirements are met. See our article on share buybacks for more details on these taxation issues.

You should obtain taxation advice from a suitable tax expert where the price paid on redemption is higher than the original issue price.

Other types of share reorganisation

For more information on other types of share reorganisations read our following articles:

This article was first published on 25 July 2018 and has been updated to reflect Companies House’s document upload process.