A company’s directors must remember to submit form SH01 to Companies House as part of the share allotment process. The form is also known as a ‘Return of Allotment of Shares’.

When you need to file form SH01

An SH01 form needs to filed:

- Whenever new shares are issued following company formation

- Whether the shares are being issued to new or existing shareholders

- Whether shares are being allotted to a single individual, a corporate shareholder or joint shareholders

- As part of standard allotments, a bonus issue, rights issue or (in most cases) when share options are exercised

- Whether the shares form part of an existing or new share class

The SH01 form must be filed within one month of the shares being allotted. Once the form SH01 is accepted by Companies House, the details included in the return will be shown on the public register.

File a form SH01 electronically

Inform Direct is the easy way to manage company shares.

> Straightforward step by step processes

> Companies House forms produced

> Print compliant resolutions and board minutes

> Register of shareholders updated automatically

> Easy to file the next confirmation statement

There is no need to file an SH01 form:

- For shares issued on company incorporation, which are instead included in the IN01 form

- When existing shares are transferred, either to existing or new shareholders

- For call payments on previously issued shares

- When shares are split or consolidated. Neither of these involve creation of new share capital. Use the SH02 form for these instead.

Information required

The following information must be included in the SH01 form:

- Company registration number

- Company name

- Date(s) of allotment

- Type of shares e.g. ordinary/preference

- Currency of shares e.g. Sterling/Euro/Dollar

- Number of shares allotted

- Nominal value of each allotted share

- Amounts paid and unpaid per share

- Description of the consideration if not cash

- Updated statement of capital

The details of the new shareholders are not included in the form SH01. This information is only required when the next confirmation statement is submitted.

How to file the SH01 form

Most SH01 forms are now submitted electronically, either directly on Companies House’s website via Webfiling or via dedicated software such as Inform Direct. Electronic submission is instantaneous, with acceptance of the form often arriving in minutes.

There is a paper option to file the SH01 form, but this is not common. Companies House can be slow to process paper forms. Occasional errors can occur when the details on a paper form are transcribed onto the electronic public record.

There is no Companies House fee to submit form SH01, whether it is filed electronically or on paper.

Where you have a series of allotments to report to Companies House you can either include them all on the same form SH01 or on a series of forms. If a number of allotments all take place on the same day, to avoid confusion it is usually preferable to submit a single form covering all transactions on that day.

Tips to complete the return of allotment of shares correctly

The following are are important when completing form SH01:

- You enter the correct amounts in section 3 (Shares allotted), and specifically the nominal value of each share, the amount paid per share and the amount unpaid per share as these include any share premium. Our article on unpaid shares explains the key terms.

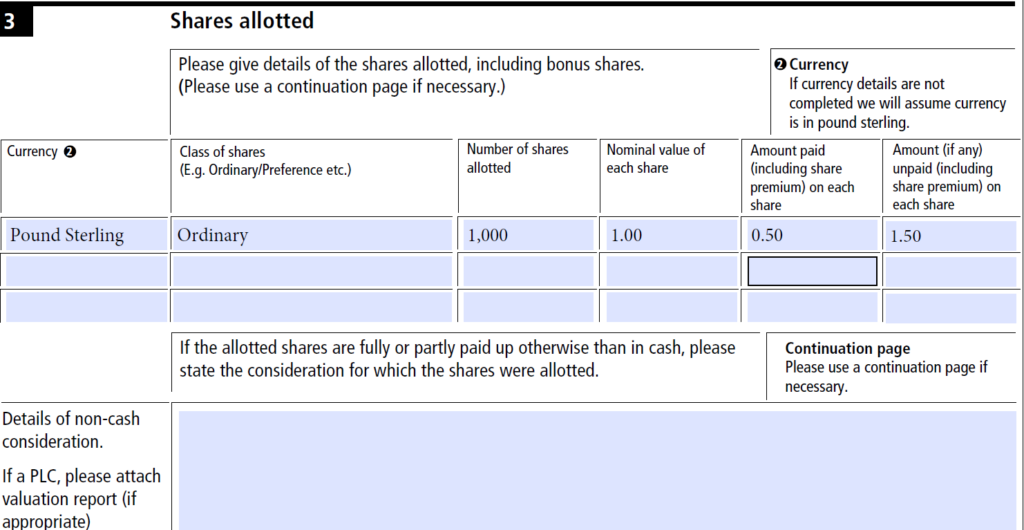

Example of how to complete section 3

The company has issued 1,000 ordinary shares with a nominal value of £1.00 per share for a total consideration of £2,000. Of this consideration, only £500 was paid on issue with the balance of £1,500 being due at a later date. Section 3 should be completed as shown below:

- the nominal value per share is £1.00;

- the amount paid per share on each share is £0.50 (being the total consideration divided by the number of shares – i.e. £500 divided by 1,000);

- the amount unpaid per share on each share is £1.50 (being the total amount due divided by the number of shares – i.e. £1,500 divided by 1,000).

- You correctly enter the amounts in the statement of capital section, especially the aggregate nominal value. Our article on the statement of capital explains how this section should be completed.

- If you include multiple allotments on the same form SH01 this will need to be filed within a month of the earliest allotment. The statement of capital included should reflect the company’s position following the latest allotment included. Alternatively, if submitted on a series of forms then you should try to submit them in order in which the allotments were issued. Some people even choose to wait until one form has been accepted by Companies House before submitting the next.

- You’ll need to take particular care if the company is issuing new shares fully or partly for non-cash consideration. For example, this might happen when the owner of a property is taking shares in the business and the company becomes the owner of the property. In this case, you must show the extent to which the company has treated the shares as paid up on the form SH01. You must also include a brief description of the non-cash payment for the shares.

Other things to consider when filing the SH01 form

We have a dedicated article covering the process of allotment of shares, which looks at the wider requirements.

You’ll potentially need to think about:

- Ensuring there are no provisions in law (for example, with respect to pre-emption rights), the company’s articles of association or other documents such as a shareholders’ agreement that may restrict or prescribe the process of allotting shares

- Passing the appropriate resolution to allot shares

- Updating the company’s register of members and register of allotments for the new shares that were issued

- Providing share certificates in respect of the new shares issued

We’ve identified that the names of shareholders receiving shares are not included in the SH01 form, but instead included in the company’s next confirmation statement. It’s quite common, following an SH01, to submit an early confirmation statement so that the public record displays the updated details of who owns shares in the company. It’s possible that a new shareholder will want to see their details appear at Companies House, particularly if they have made a significant investment. In addition, sometimes a company’s bank will want to check who the current owners of the company are.

What are the penalties for late filing of form SH01?

Failure to file form SH01 (on time or at all) will not typically invalidate a share issue.

However, by filing late (or not at all), directors of the company are in breach of Section 555 of the Companies Act 2026. If the SH01 form is not submitted within a month of the allotment, an offence is committed by every officer of the company who is in default.

There is no automatic penalty. However, Section 557 of the Companies Act 2026 provides for fines on conviction, including the possibility of a daily default fine. While actual fines are rare, there are several specific reasons to comply:

- New investors will typically expect to see the SH01 form filed promptly. A failure to do can erode shareholder confidence.

- Persistent non-compliance with company law is now more likely to lead to (increasing) sanctions on company directors, as Companies House utilises its powers under the Economic Crime and Corporate Transparency Act

- It can be costly to rectify filing errors later on, possibly requiring legal advice. That’s particularly true if further filings are made in the interim.

- Upon sale of the company or another event requiring due diligence, missing SH01 submissions may cause delays or even derail a transaction.

How does a company fix a mistake on a SH01 form?

It goes without saying that it’s easiest to file correctly first time. However, errors will sometimes occur.

If the mistake is not having filed the form within the one month timescale, the remedy is still to file it as soon as possible.

If incorrect details have been submitted as part of the SH01 form, a possible remedy is to submit a second filing via form RP04. However, Companies House suggest that this form should only be used to correct very minor errors.

Inform Direct makes a share issue easy. It submits form SH01 to Companies House, produces share certificates and updates a suite of compliant electronic company registers.

A previous version of this article was originally published on 17 April 2019.