Authorised share capital defined a maximum value of shares that a company could issue. Until 2009 it was compulsory to include it in the memorandum of association. After 2009 it is no longer required to have a limit on share capital, but it is still possible to set one in the company’s articles. Here we examine the historic concept of authorised share capital, how it used to operate, and how it can still affect companies today.

Background

Any limited company incorporated before the 1st of October 2009 may still have an out-of-date clause lurking in its memorandum of association. Before that date, the memorandum had to contain statements defining the ‘authorised share capital’: the maximum nominal value of a company’s shares. It was also necessary to fix the number of shares and the value of each share.

For example, the company’s authorised share capital might be fixed at £20,000 divided into 20,000 shares of £1 each. Share capital was a finite pool from which new shares could be issued, whereas after 2009 the pool is effectively infinite.

This limited amount of authorised share capital was written into the new company’s memorandum of association, forming part of the company’s constitution and therefore becoming a rule which its directors must follow.

Need enhanced articles of association for your company?

Our professionally drafted articles of association offer various enhancements upon the standard Model Articles, offering tailored support whether you have one, two or three share classes.

You can purchase these enhanced articles online for your new or existing company.

Why did authorised share capital exist?

This rigid fixing of maximum share capital stems from the days when stamp duty was payable upon registration of a new company. The higher the share capital, the higher the stamp duty. New companies would limit their share capital to reduce the stamp duty bill upon incorporation.

It was a similar situation to the early days of motoring, when taxable horsepower was calculated not on actual engine power but on cylinder dimensions, specifically the bore diameter. The result was cars with engines whose cylinders had a long stroke and a narrow bore. Cars were built like that to avoid high tax. In the same way, companies were built to avoid high stamp duty.

A limit to authorised share capital also reassured shareholders that their holdings would not be unacceptably diluted by the issue of shares beyond the defined amount.

Without a fixed limit to its share capital, there would have been nothing to prevent companies from incorporating with a minimal share value and then issuing and allotting freely afterwards, once the stamp duty had been paid on its incorporation documents. A set amount of authorised share capital served to thwart this tax dodge.

A limit to authorised share capital also reassured shareholders that their holdings would not be unacceptably diluted by the issue of shares beyond the defined amount.

Even if they enjoyed shareholder pre-emption rights, they would usually only be given first refusal over enough further shares to maintain their percentage stake in the company. For example, a shareholder with 25% of issued shares would only have first refusal on 25% of any new shares. This was a statutory right under the 1985 Act, and continues to be so under the 2006 Act. However it can be altered or disapplied in a company’s articles of association.

Existing shareholders may have preferred not to have to engage in such a share ‘arms race’ just to maintain their percentage stake. A fixed issuable share capital gave subscribing shareholders a measure of security in this regard.

Cars were built like that to avoid high tax. In the same way, companies were built to avoid high stamp duty.

The authorised share capital could only be increased (or indeed decreased) via a special resolution passed by the shareholders and a notification to Companies House.

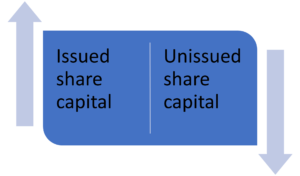

A company did not have to issue and allot all the shares in its authorised share capital. When a decision was taken to issue new shares, they had to be taken from the company’s limited pool of ‘unissued share capital’.

In the minds of directors of companies formed under the 1985 Act, two quantities existed in their share capital position: unissued share capital and issued share capital. Share capital was a closed system in which the proportional quantities could vary but the total always remained the same.

In our example above, the company is set up with an authorised share capital of £20,000. If £5,000 worth of shares are in issue, the unissued share capital is £15,000. If a further £3,000 of shares are issued, the unissued share capital falls to £12,000 and the issued share capital rises to £8,000. Once the unissued share capital fell to zero, no further shares could be issued. Any attempt to issue shares beyond the authorised limit could be declared void.

By the time of the 2006 Companies Act, authorised share capital had come to be seen as largely unnecessary, a source of confusion, and a case of overkill. Shareholders can voluntarily stipulate a limit on share capital at any time via an ordinary resolution, which has the same effect as a statement of authorised share capital in the original memorandum and/or articles.

By the time of the 2006 Companies Act, authorised share capital had come to be seen as largely unnecessary, a source of confusion, and a case of overkill.

Why might it matter?

Many companies incorporated under the Companies Act 1985 may still have provisions for authorised share capital in their memoranda of association. If share reorganisations have been rare or absent during the company’s history, the board may be unaware of any limitation on share capital and risk falling foul of their own rules in the event of attempts to issue and/or allot further shares.

What to do about it

There is a lack of legal certainty over whether an ordinary resolution is enough to remove a pre-existing provision from a company’s memorandum following the transitional period between the 1985 and 2006 Companies Acts.

For that reason, any company incorporated prior to October 2009 and wishing to remove provisions for authorised share capital from its original memorandum of association should consider passing a special resolution to adopt new articles that do not include the old requirement.

A special resolution requires a vote of 75% in favour and Companies House must be notified within 15 days of the date of the resolution’s passing. There is no statutory form for this. Companies House suggests a simple document bearing company number and name, the details of the meeting and resolution, and the signatures of the directors or those acting on behalf of the company.

We provide this template as a starting point: Shareholders’ resolution to remove authorised share capital restriction. This will work as a quick fix, but in this situation many companies will consider adopting new articles which bring this and other issues of corporate governance up to date.

As with any major rearrangement of a company’s constitution, professional legal and/or accountancy advice should be sought before taking any action. Companies with multiple share classes or a single director may wish to consider Inform Direct’s Enhanced Articles of Association, which make provisions to clarify these and other areas of ambiguity in the model articles.

For a quick guide to changing a company’s articles of association and reporting the special resolution required to do so, see our article on how to change a company’s articles of association.

There is no requirement to remove pre-2009 statements about authorised share capital from a company’s memorandum of association, and some companies may prefer to leave things as they are.

Prior to the 2006 Act a company’s memorandum of association would be the place to look for details of authorised share capital. But the 2006 Act moved the company’s rules from the memorandum to the articles of association. The memorandum is now a much sparser document, merely declaring a wish to form a company under the 2006 Act, to agree to become members of the company, and to take at least one share each.

This means that matters pertaining to shares are now to be found in the articles of association, and it is these that will contain any new statements about share capital.

Best practice before any new share allotment is to check the memorandum of association for any provisions about authorised share capital. If these exist and it is desired to issue new shares which would mean exceeding the authorised share capital, envisage a special resolution to adopt new articles which permit issuing the new shares, seek advice, and inform Companies House of the new articles within 15 days of their adoption.