A micro-entity is a very small company or LLP. We will define the criteria for micro-entity status below. Micro-entities may be able to produce a much simpler set of year end accounts for their members and provide less information for the public record.

Why did the Government create the new micro-entity classification?

When the UK Government approved The Small Companies (Micro-Entities’ Accounts) Regulations 2013, the Department for Business, Innovation & Skills released the following statement:

Micro-entities are, in many instances, effectively owner-managed. Statutory financial statements of micro-entities, therefore, may not need to facilitate communication between shareholders and management in relation to the company’s performance. For the smallest of companies, the burdens associated with comprehensive financial reporting requirements may be disproportionate when compared with other small companies.

What is the aim of the micro-entity regime?

The aim of the micro-entity regime is to save the very smallest of businesses both time and costs by:

- Offering a highly simplified format of statutory accounts containing fewer elements than a full set of company accounts.

- Simplifying the accounting standards that should be applied such that they will be more widely understood and with less specialised knowledge required.

Ready to file micro-entity accounts?

Inform Direct provides a simple and efficient approach to the task of producing fully compliant micro-entity accounts for private companies limited by shares or guarantee.

How does a company qualify as a micro-entity?

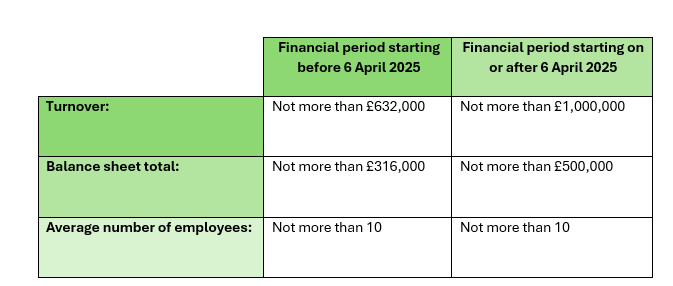

Section 384A of the Companies Act 2006 sets out the criteria that a company must meet in order to qualify as a micro-entity, including a requirement that it be within at least two of the three size thresholds disclosed in the table below. The thresholds were updated by The Companies (Accounts and Reports) (Amendment and Transitional Provision) Regulations 2024, with the new increased size thresholds applying for accounting periods starting on or after 6 April 2025:

When determining company size, The Companies (Accounts and Reports) (Amendment and Transitional Provision) Regulations 2024 allow companies to take advantage of the increased size thresholds as soon as possible. Companies reporting a financial period that starts on or after 6 April 2025 can treat the new higher size thresholds as if they applied for the previous accounting period. This is important as the company may need to meet the size qualification criteria for two consecutive financial years. Refer to our guide on how to calculate company size for year end accounts preparation for more details.

Notes regarding calculation of key company size thresholds:

1 Turnover

This threshold should be proportionately adjusted if the accounting period is shorter or longer than 12 months. For example, for a nine-month accounting period commencing on or after 6 April 2025 the new uplifted turnover threshold would be reduced to £750,000 (being 9/12 of £1,000,000).

2 Balance sheet total

The total of the amounts shown as assets on the balance sheet as at the accounting reference date.

3 Average number of employees

Section 384A(7) provides guidance on how to calculate this figure.

The ‘two years in, two years out’ rule

If this is the company’s first financial year and the company is within at least two of the three size thresholds, then it may qualify as a micro-entity. For subsequent years, however, the rules are more complex and are explained in our guide entitled How to calculate company size when preparing year end accounts, including a flowchart showing how to navigate the potential complexities of the ‘two years in, two years out rule’.

Are some types of company excluded from being treated as micro-entities?

Helping you manage your companies, whatever their size

An important part of managing a company is keeping statutory books and Companies House filings up to date.

Inform Direct is the perfect tool to make this task a whole lot easier, meaning you can focus more on running your business.

Even if your company qualifies on the basis of size, the nature of the company’s business may exclude it from being treated as a micro-entity.

Section 384B excludes the following from being treated as micro-entities:

- Any company excluded from being treated as a small company as per section 384 of the Companies Act 2006.

- Investment undertakings, financial holding undertakings, credit institutions and insurance undertakings.

- Charities.

- Overseas companies.

- Limited partnerships.

- Public limited companies.

- Unregistered companies.

What about group companies?

There are further exclusions if the company is part of a group. Micro-entity provisions cannot be applied if:

- The company is a parent company which prepares group accounts, then it cannot produce its individual accounts using micro-entity provisions.

- The company is part of a group and its accounts are included in consolidated group accounts.

Can LLPs prepare and file micro-entity accounts?

Yes. Regulation 6 of The Limited Liability Partnerships, Partnerships and Groups (Accounts and Audit) Regulations 2016 states that:

Sections 384A and 384B(1) [of the Companies Act] apply to LLPs.

Qualification is by meeting the same company size criteria already detailed in this article and by ensuring that the LLP does not undertake any ineligible business or form part of a group.

Is a company that qualifies as a micro-entity required to adopt the micro-entity regime?

No. A company’s managers may always choose to prepare and file year end accounts that provide more than the minimum required disclosure (by adopting a financial reporting regime that would apply to larger companies). Indeed, there are both advantages and disadvantages to opting for the reduced disclosure requirements that apply when preparing micro-entity accounts, and these should be carefully weighed.

What are the advantages of preparing micro-entity accounts?

The main advantages of preparing micro-entity accounts are:

- Highly simplified presentation of the balance sheet and profit and loss. The company may choose from two different formats for the balance sheet and only one format for the profit and loss account.

- No requirement to prepare a directors’ report. This requirement was removed for micro-entities by section 415 (1A) of the Companies Act 2006.

- No detailed notes to the accounts required. Instead, details are only required of certain ‘minimum accounting items’ – and these should be disclosed at the foot of the balance sheet.

- Accounts are presumed to give a true and fair view. This contrasts with accounts prepared under the small companies’ regime which require a degree of appraisal to ensure that they present a true and fair view despite limited disclosure requirements.

- Accounts can be ‘filleted’. There is no requirement to file the profit and loss account for the public record. However, note that the Economic Crime and Corporate Transparency Act 2023 (ECCT Act) will soon require all companies, including micro-entities, to file a profit and loss account.

- Significant simplifications to recognition and measurement requirements. For example, the accounting for financial instruments has been simplified whilst the need to account for deferred tax is not required (or indeed allowed).

These advantages mean that a decision to prepare micro-entity accounts is likely to save the company both time and money. Moreover, with less disclosure required for the public record, less company information will be available to competitors.

Why might a company choose not to prepare micro-entity accounts?

It might not always be advantageous for an entity to opt for the reduced accounting disclosure allowed by the micro-entity regime. For example, you should consider the following:

- Will micro-entity accounts provide enough information? Far less detail is provided in a set of micro-entity accounts as compared to accounts produced under the small companies’ regime. This reduced disclosure may not be sufficient for current or future lenders and creditors, for credit rating agencies or for shareholders. Additional costs may therefore arise if any of these agencies request additional information. It may be difficult to secure new investment or shareholder funding without providing more financial details than those given in micro-entity accounts.

- Will the company be able to prepare micro-entity accounts next year? It may not be appropriate to prepare micro-entity accounts for a company that is growing very quickly and that is unlikely to qualify to prepare accounts under the same regime in the near future.

- Will the available accounting formats be flexible enough? Only one format of profit and loss account is allowed (Format 2), and whilst two formats of balance sheet are available, asset and liability classes are highly summarised and cannot be analysed out into further detail. For example, there is only one line item for fixed assets and this cannot be analysed into intangible assets, fixed assets and investment property.

- Will the accounts give an accurate presentation of the company’s position? The highly summarised format, particularly when accompanied by a move away from the use of accounting expertise, may increase the risk of the accounts providing an inaccurate or misleading picture of the company’s true position.

- What impression of the company might micro-entity accounts give? In some industries and for some companies, choosing to file more detailed accounts may give a sense of prestige or status to the company.

- Will the removal of accounting policy options present a problem? In order both to simplify their preparation and to deal with the lack of explanatory notes in a set of micro-entity accounts – many accounting policy options have been removed. For example, FRS 105 (the financial reporting standard that must be applied by micro-entities) does not allow the recognition of deferred tax, and the following commonly adopted accounting treatments are also disallowed:

Assets carried at fair value or revaluation

A micro-entity that has an investment property currently valued at fair value or open market value would have to restate the value of the property to cost. In addition, if the company has not been reflecting depreciation because it has been revaluing the property, FRS 105 would require that all depreciation accumulated since the date of acquisition of the property now be reflected in the micro-entity accounts. The inclusion of a revaluation reserve on the balance sheet would not be allowed.

In these circumstances a decision to prepare micro-entity accounts could result in a significant change to the company’s balance sheet position.

Capitalisation of development costs and borrowing costs

A company that has in the past capitalised development and/or borrowing costs is not allowed to do so when preparing micro-entity accounts. Instead the previously capitalised costs must be expensed to the profit and loss account.

What financial reporting standard should be used when preparing micro-entity accounts?

Companies choosing to apply the micro-entities regime must apply FRS 105, The Financial Reporting Standard applicable to the Micro-entities Regime when preparing their statutory accounts.

If the company chooses to include information in addition to the ‘minimum accounting items’ required in their micro-entity accounts, then for these additional disclosures the company must refer to section 1A of FRS 102.

What elements must be included in a set of micro-entity accounts?

A full set of micro-entity accounts includes the following elements:

- Simple balance sheet and footnotes.

- Signature of a director and their name printed on the balance sheet.

- Statement on the balance sheet above the director’s signature that the accounts have been prepared in accordance with the micro-entity provisions.

- Simple profit and loss account.

- Auditors’ report. However, in reality most micro-entities will be able to claim exemption from audit.

At the time of publication a micro-entity can choose to prepare and file abridged accounts in accordance with the provisions of section 444 of the Companies Act 2006 , and thereby elect not to file the profit and loss account and any supporting notes related to the profit and loss account. Note however, that the provisions of the ECCT Act will soon abolish abridged accounts and all micro-entities will then be required to file their profit and loss account (also known as the income statement).

What are ‘minimum accounting items’?

No disclosure notes are required to support micro-entity accounts. However, details of any off balance sheet arrangements, advances, credit or guarantees granted to directors, other financial commitments, charges, contingent liabilities and guarantees, as well as the average number of employees must be disclosed at the foot of the balance sheet. These items are referred to as the ‘minimum accounting items’. For more details of these required disclosures refer to section 6 of FRS 105.

Can micro-entity accounts be submitted to HMRC?

Yes. Micro-entity accounts that have been prepared using the provisions of the micro-entities regime and following the accounting guidelines set out in FRS 105 can be submitted to HMRC as part of your company’s annual tax return. Note however that you must include the profit and loss account, even if you removed this when filing with Companies House.

If you use Inform Direct to file micro-entity accounts, then we will also provide an IXBRL-tagged version of the accounts that can be included with the corporation tax return (CT600) that you file separately with HMRC outside of Inform Direct.

What are the alternatives for a company choosing not to apply the micro-entities regime?

If an eligible company chooses not to apply the micro-entities regime (and FRS 105) then in practice they will usually choose to apply the small companies’ regime and the accounting guidelines set out in FRS 102 (and particularly Section 1A for small entities).

What statements should be included on the balance sheet of a micro-entity?

Most very small companies using the micro-entity regime will be exempt from audit and will be filing unaudited accounts. These companies should include the following statements on their balance sheet, in a prominent position above the director’s signature:

Statement that the accounts have been prepared under micro-entity provisions:

“These accounts have been prepared in accordance with micro-entity provisions.”

Statements when the company is entitled to audit exemption:

“The directors consider that the company is entitled to audit exemption under Section 477 of the Companies Act 2006 for the year ended [insert year end].”

“The members have not required the company to obtain an audit of its accounts for the year ended [insert year end] in accordance with Section 476 of the Companies Act 2006.”

“The directors acknowledge their responsibilities for complying with the requirements of the Companies Act 2006 with respect to accounting records and the preparation of accounts.”

Statement that the profit and loss account has not been delivered:

“These accounts have been delivered in accordance with the provisions applicable to companies subject to the small companies’ regime. The profit and loss account has not been delivered to the Registrar of Companies in accordance with special provisions applicable to companies subject to the small companies’ regime.”

Our streamlined wizard for efficient micro-entity accounts production makes it easy to get it right first time.

Earlier versions of this article were published in October 2018 and June 2022. The latest updates were applied in May 2025.