This guide will help you understand the income statement (profit and loss account) for small companies and micro-entities. It covers how to get your income statements filed on time with Companies House and HMRC and be compliant with the latest rules.

What is an income statement?

An income statement, also known interchangeably as a profit and loss account, provides a summary of a company’s revenues, expenses, and profits over a specific period. It shows both turnover and profitability for the company over that length of time. This contrasts with the balance sheet, which is a snapshot of a company’s overall financial position at a given moment.

How are income statements used?

The income statement helps stakeholders assess a company’s profitability and efficiency. Interested parties such as investors, creditors and management will read and analyse it. They are likely to use it in one or more of the following areas:

Streamline your Companies House accounts

Inform Direct makes it easy to:

> Prepare and file fully compliant accounts

> Get it right first time and reduce rejections

> Only file what Companies House needs

> Automate micro-entity & dormant accounts

- Financial performance assessment. It gives a straightforward picture of whether the company has made a profit or a loss over this year, and how this compares to the previous year.

- Decision making. The income statement helps owners and managers make informed decisions about pricing, cost control, and resource allocation. For example, if the income statement shows consistent losses, this will inform a decision to adjust prices or cut costs.

- Tax reporting. The income statement provides a breakdown of revenues, expenses, and net income (profit or surplus), which is essential for accurate tax reporting.

- Attracting investment. Investors and lenders will typically ask to see financial statements, including the income statement, to assess the company’s financial health and its ability to repay loans or provide a return on investment.

What types of companies are required to file an income statement at Companies House?

Large and medium companies

Large and medium companies are required to file full accounts that require professional preparation. These include a balance sheet and statement of cash flows accompanied by an income statement, as well as detailed notes to the accounts, an auditor’s report and a directors’ report. See more on this in our article Types of limited company accounts and the details they should include.

LLPs

LLPs (limited liability partnerships) of all sizes, now including micro-entities (subject to secondary legislation following the Economic Crime and Corporate Transparency Act (ECCTA)) are required to file an income statement.

Small companies

At some point after ECCTA, probably in early 2025, small companies will become required to file a full balance sheet, income statement and director’s report. Abridged and ‘filleted’ accounts will no longer be allowed.

Micro-entities

Following the ECCTA, micro-entities will need to start including an income statement (profit and loss account) alongside ain their annual accounts filings with Companies House. A directors’ report will remain optional for micro-entities. Previously micro-entities were only required to file a simplified of the balance sheet.

The exact timeline for the introduction of these changes is yet to be established. Ultimately, though, they will lead to income statements being a requirement for all sizes of company, including micro-entities. Coupled with a move towards mandatory accounts filing via software with iXBRL tagging, this will enable more detailed cross-checking of accounts with HMRC. The intention is to facilitate the discovery of irregularities that could be linked to economic crime.

For other accounts changes following the Economic Crime and Corporate Transparency Act (ECCTA), please see our article Navigating the ECCT Act: changes to accounts filing at Companies House.

What do income statements contain?

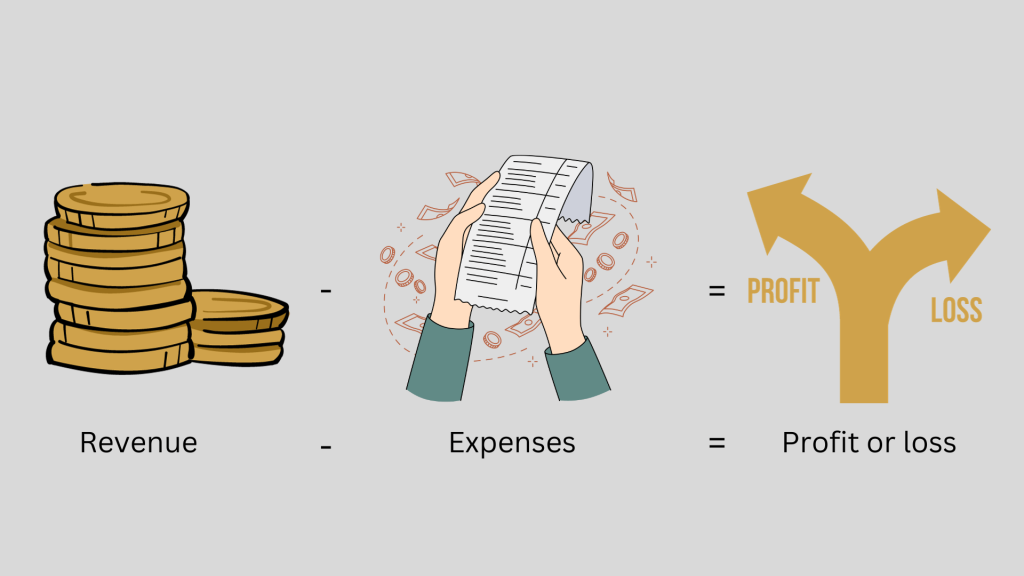

The income statement shows what is left over after expenses are subtracted from income.

The main elements typically found in an income statement all contribute to this equation. For a micro-entity (the most common type of company as well as the simplest for accounting purposes) the following elements are typical:

Income

Turnover: The income a company earns by providing goods and services in its usual trading. For businesses registered for VAT, turnover should be recorded after the deduction of VAT (‘net of VAT’).

Other income: Any income that is not part of turnover, i.e. does not come from sales. It can include interest earned on investments, rent, the sale of assets and many other forms of income that did not originate from selling products and services.

Expenses

Cost of raw materials and consumables: Costs related to producing the products or services but not including staff costs. For a company making ceramic pots this might include clay and glazes; for a service company it may include administrative costs, service fees, stationery and insurance.

Staff costs: Salaries and wages, pension costs, National Insurance contributions, payroll costs, travel expenses and other expenses directly related to the employment of staff.

Depreciation and other amounts written off assets: Depreciation is the amount charged to the income statement in one year for a fixed asset that is being written off over multiple years. It spreads the cost of acquisition over the useful life of the asset. For example, a company buys an industrial printer that costs £15,000. The useful life of the printer is estimated to be ten years. Each year for the next ten years, £1,500 will be charged to the income statement under depreciation. This amount is simultaneously removed from the balance sheet.

This method ensures that the expenses related to an asset are recognised over its useful life, leading to more accurate financial statements. The asset’s value on the balance sheet is reduced each year, which reflects its worth to the company more accurately than a single lump sum payment in the year it was acquired.

Businesses can often claim tax deductions for depreciation expenses, which can lower their taxable income and consequently their tax liability.

When applied to intangible assets, this process is called amortisation.

Other charges: Expenses that do not fall into any other expense category.

Tax: The estimated corporation tax payable on the company’s profits or losses during the accounting period. Profits are income less expenses, but HMRC might arrive at a different figure than the estimate because not all expenses are deductible for tax purposes.

Profit/Loss (sometimes referred to as Surplus/Deficit): this final figure shows the profit or loss the company has made during this particular accounting period.

Income statement example

The income statement is usually presented as two columns, one for the previous year and one for this year, to allow easy comparison. Figures are in pounds sterling. Negative values like costs and expenses are shown in brackets. Here’s how it might look for a micro-entity:

Bob’s Bobbins Ltd.

Income Statement

for the year ended 31 December 2023

| 2023 | 2022 | |

|---|---|---|

| £ | £ | |

| Turnover | 412,365 | 347,219 |

| Other income | 1,554 | 1,819 |

| 413,919 | 349,038 | |

| Cost of raw materials and consumables | (167,980) | (159,152) |

| Staff costs | (52,500) | (43,500) |

| Depreciation and other amounts written off assets | (7,500) | (3,500) |

| Other charges | (28,645) | (27,300) |

| Tax | (7,684) | (11,001) |

| Surplus | 149,610 | 104,585 |

When and where should I send the income statement?

Companies House: As part of a private limited company’s first accounts with Companies House, the deadline is 21 months after the company’s registration date. For annual accounts after the first ones, the deadline is 9 months after the end of the company’s financial year.

HMRC: A tax return that includes the income statement must be filed within 12 months of the end of the company’s accounting period for Corporation Tax.

You must pay Corporation Tax or tell HMRC that you don’t owe any within 9 months and 1 day of the end of the company’s accounting period for Corporation Tax.

How does the income statement differ from the balance sheet?

| Income statement (profit & loss account) | Balance sheet | |

|---|---|---|

| Purpose | Shows how much revenue the company earned, what expenses were incurred in generating that revenue, and whether the company made a profit or a loss during an accounting period. | Shows what the company owns, what it owes, and what is left after accounting for liabilities. |

| Time frame | Covers a specific time period, usually a year, although with the agreement of Companies House the reporting period can be longer or shorter than this. | Reflects the financial position of the company at a specific moment in time, usually at the end of a reporting period such as a financial year. Provides a static picture of the company's financial situation. |

| Content | Includes turnover (sales), other income, various types of expenses and taxes, and the resulting net income (profit or loss). | Includes assets, liabilities, and equity. Assets are what the company owns, liabilities are what it owes, and shareholders' equity represents the residual interest of the owners in the company's assets after deducting its liabilities. |

What useful financial indicators can be calculated from the income statement?

From an income statement and balance sheet, you can calculate and infer various key performance metrics that offer insights into a company’s profitability, efficiency, and overall financial health. Here are some common quantities and ratios that can be inferred from an income statement when combined with quantities from the balance sheet:

Net profit margin: this is the bottom-line profitability ratio, measuring the percentage of turnover that remains as net income after all expenses, including taxes, have been subtracted.

Net income growth rate: This shows the percentage increase or decrease in net income from one period to another, providing insights into a company’s growth trajectory.

Return on assets (ROA): It measures how efficiently a company uses its assets to generate profit. It’s calculated as profit / total assets.

Return on equity (ROE): ROE measures how effectively a company uses shareholders’ equity to generate profits. It is calculated as net profit / shareholders’ equity.

Tax Rate: Calculate the effective tax rate by dividing tax expense by pre-tax income.

For financial indicators that can be calculated from the balance sheet, please see our article what is a balance sheet?

"The offering by Inform Direct is complete, professional and incredibly efficient"- Dan Edwards of Veritons Limited