The Companies Act 2006 may allow you to prepare and file a simpler set of year end accounts, dependent upon your company’s size. But how do you determine what size your company is for the purposes of accounts preparation?

There are two conditions that you must consider when determining whether your company qualifies for any of the simpler year end accounts formats. These are:

1. Eligibility

Whether your company meets the eligibility criteria that may allow it to qualify for reduced accounting disclosure based on size.

2. Company size

What size your company is for the purposes of year end accounts preparation and filing.

For eligible companies that can be classified as micro-entities, or small or medium-sized companies, it may be possible to prepare a less detailed set of year end accounts containing fewer elements, both for members and for filing on the public record. Companies classified as large will not have access to any exemptions and must prepare a comprehensive set of year end accounts that meet the disclosure requirements in full.

The regulations

Determining whether your company might qualify for exemptions from full disclosure requirements when preparing year end accounts is not straightforward. The rules set out in the Companies Act 2006, and amended by The Companies, Partnerships and Groups (Accounts and Reports) Regulations 2015 are complex.

To help you through the decision process, this article contains two simple flow charts to walk you through the factors you should consider when determining both the size and the eligibility of your company. However, if in doubt, we would always advise you seek further guidance from an accounting professional.

Helping you manage your companies, whatever their size

An important part of managing a company is keeping statutory books and Companies House filings up to date.

Inform Direct offers a simple and efficient approach to the task of producing fully compliant micro-entity accounts for private companies limited by shares or guarantee.

The information that follows considers standalone company accounts only and will not look at the additional provisions surrounding the preparation of group accounts.

Eligibility first

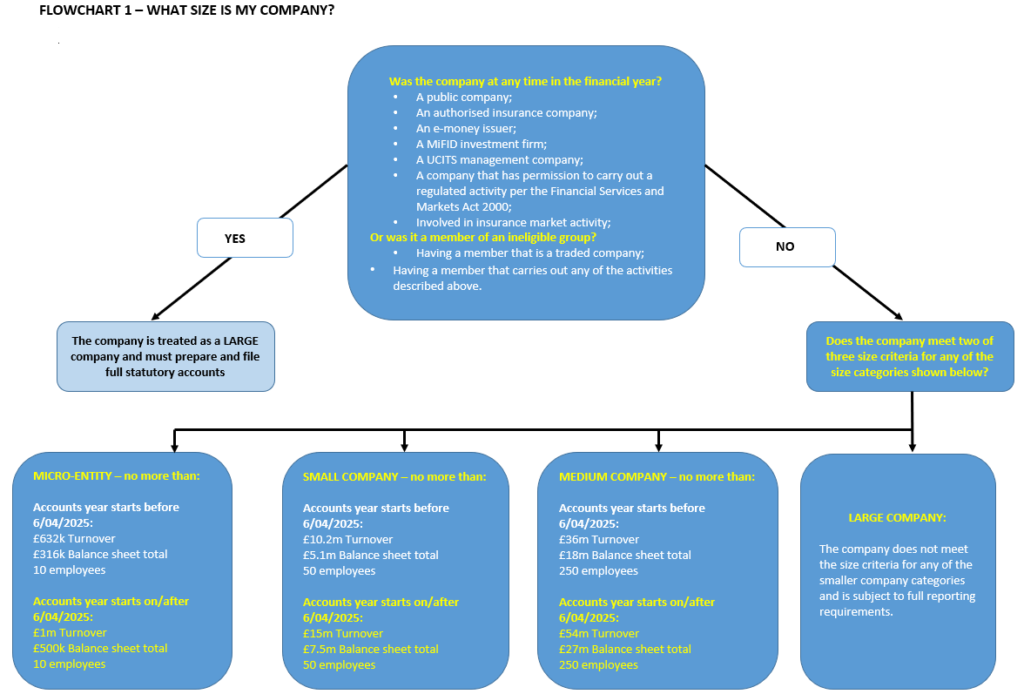

There are certain types of company that never qualify for reduced disclosure, even if they meet the company size thresholds for a micro-entity, small or medium-sized company. These companies, defined in sections 384 and 467 of the Companies Act 2006, are excluded from the small companies’ regime or from being considered medium-sized companies. They are always treated as large companies, and as such must prepare and file a full set of year end accounts, with no accounting exemptions available.

To determine whether your company may qualify to prepare a simpler set of annual accounts, consider FLOW CHART 1. The flowchart begins by listing the types of companies that are excluded from the possibility of applying accounting exemptions. If your company is not one of these special types of company, it has passed the first eligibility test and you can now move on to consider company size.

Determine company size

Consider the company size thresholds illustrated in FLOW CHART 1.

To qualify for a company size threshold (micro-entity, small or medium-sized company) for the year to which the accounts are being prepared and filed, the company must not exceed at least two of the three stated size criteria. If the company does exceed two or more of the size criteria, for all the company size classifications, then for that accounting year it will be classified a large company – although as we explore later in this article, if this is not the company’s first accounting period it may still be possible to file a simpler set of year end accounts. The size thresholds were increased with effect from 6 April 2025. The uplifted size thresholds apply to accounting periods that start on or after 6 April 2025.

When using the flow chart to determine whether your company is within any of the company size boundaries for the accounting period, you should be aware of the following provisions set out in the Companies Act 2006:

- Where the company’s accounting period is not actually a year – the maximum figures given for the criteria ‘Turnover’ may be ‘proportionately adjusted’. To illustrate: if your accounting period is in fact 15 months long, then the maximum ‘Turnover’ figure may be uplifted by 15/12 for the purposes of determining whether that condition can be met. Similarly, a nine-month accounting period would produce a reduced turnover threshold value equal to 9/12 of the statutory threshold amount.

- The balance sheet total refers to the total of the ‘amounts shown as assets in the company’s balance sheet’.

- The number of employees refers to the average number of persons employed by the company in the accounting period. Section 382 of the Companies Act 2006 prescribes the method of calculating this average.

- Where group accounts are to be prepared, different size thresholds apply. These are set out in sections 383 and 466 of the Companies Act 2006.

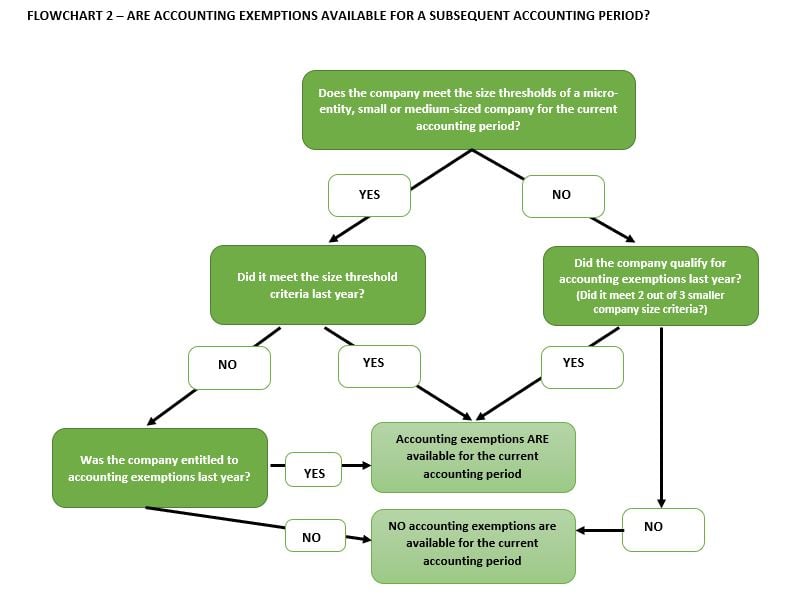

Subsequent accounting periods

If this if the company’s first financial reporting period, then application of the company size thresholds is very straightforward. The Companies Act 2006 states that a company will qualify as small or medium-sized, if the

qualifying [size] conditions are met in that year.

However, for succeeding years, a more complicated two-year rule applies. Section 382 (2) of the Companies Act 2006 states that in subsequent years

where on its balance sheet date a company meets or ceases to meet the qualifying [size] conditions, that affects its qualification as a small company only if it occurs in two consecutive financial years

Application of the ‘two consecutive financial years’ rule can be tricky, so FLOW CHART 2 has been designed to illustrate the logic. However, it may be advisable to consult an accountant if in any doubt.

The effect of increased company size thresholds on the “two-year rule”

The company size thresholds were uplifted with effect from 6 April 2025. Transitional provisions set out in The Companies (Accounts and Reports) (Amendment and Transitional Provision) Regulations 2024 enable companies to take early advantage of the increased thresholds. Companies reporting a financial period that starts on or after 6 April 2025 can treat the new higher size thresholds as if they also applied for the previous accounting period, when they are determining whether they meet the size thresholds for two consecutive financial periods.

Having determined whether your company is eligible to prepare one of the simpler year end accounts formats with reduced accounting disclosure, you may wish to read our related article Types of limited company accounts and the details they should include. This guide explores the different types of year end accounts that can be prepared and filed, and the elements and details you should include if your company qualifies as a micro-entity, small, medium-sized or dormant company.

File company accounts on time and keep statutory books up to date. It's quick and simple with Inform Direct.

An earlier version of this article was published on 3 August 2018. A full update was applied on 7 May 2025.