Every year, companies must prepare statutory accounts for their members and must also file a version of these with Companies House. However, dependent upon the type and size of the company, different limited company accounts formats may be available.

Company size thresholds

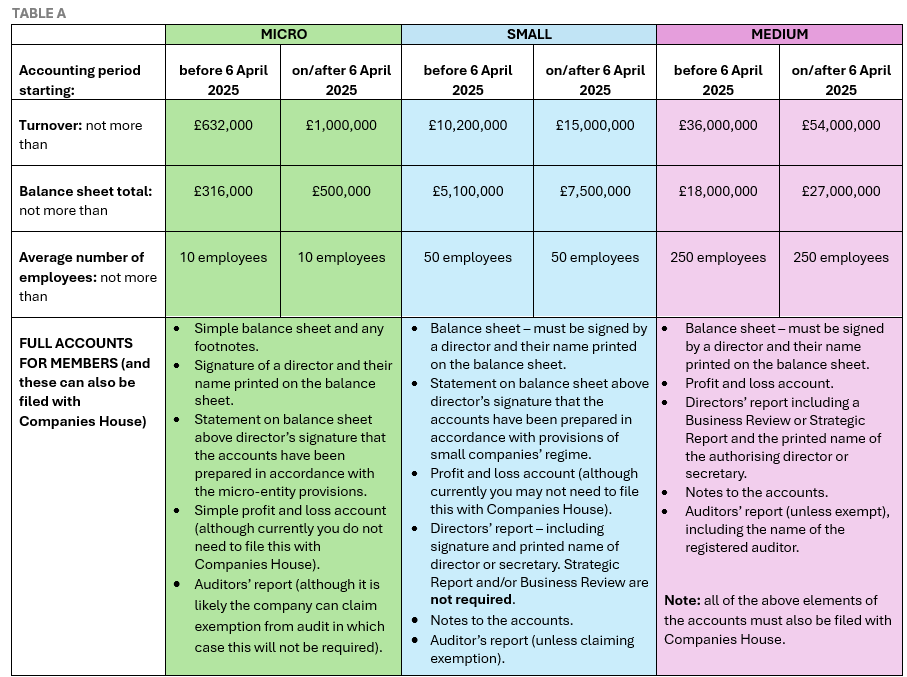

The Companies Act 2006 prescribes a set of thresholds that determine the size of a company. These thresholds are important because they decide the amount of detail a company must include in it’s statutory accounts. A company can be classified as very small (a micro-entity), small or medium. If it does not qualify for any of these size standards, then it is considered a large company, and as such must prepare and file a full set of limited company accounts. The elements that are included in a full set of company accounts are set out in section 3.1 of the guide ‘Preparing and filing Companies House accounts’, including:

- A full balance sheet signed by a director on behalf of the board;

- A full profit and loss account;

- A comprehensive set of notes to support the balance sheet and profit and loss account;

- A directors’ report signed by a director (or company secretary);

- a strategic report; and

- An auditor’s report.

However, companies that qualify as micro-entities, small or medium-sized, may be eligible to produce and submit year-end accounts that are simpler and contain fewer elements.

To qualify for a particular size classification, the company must meet at least two of three size thresholds. Be careful to apply the correct set of size thresholds, as determined by the starting date of the financial period. The Companies (Accounts and Reports) (Amendment and Transitional Provision) Regulations 2024 introduced uplifted thresholds for accounting periods that start on or after 6 April 2025. All the company size thresholds are set out in Table A below:

The two year rule:

If this is the company’s first financial year then it is straightforward to calculate company size for the purposes of accounts preparation. For most companies, (there are some limited exceptions dependent upon the trading activity of the company) it is as simple as meeting the size classifications outlined in the table above. For subsequent years however, the rules are more complex and are explained in our guide entitled How to calculate company size when preparing year end accounts.

Full accounts

The elements that make up a full set of limited company accounts vary, dependent upon the size of the company. As can be seen from Table A – the smaller the company classification, the less detail is required in a full set of limited company accounts. The smallest companies can prepare micro-entity accounts – a special type of full accounts, that need only contain a simplified balance sheet with footnotes and a simplified profit and loss account. Under section 477 of the Companies Act 2006, most micro-entities and small companies will also be able to claim exemption from audit and will not therefore be required to submit an auditor’s report.

As has already been mentioned, no exemptions are available to large companies.

It is possible that the company may not be required to submit a full set of accounts to Companies House, although again this is dependent upon the size of the company. There are simpler options that may be available and we move on to consider these now.

Abridged accounts – for small companies only

Currently, small companies have the option to prepare abridged accounts. Abridged accounts are only available to companies that are entitled to prepare accounts under the provisions of the small companies’ regime (as defined in section 381 of the Companies Act 2006). Micro-entities, medium-sized and large companies are not eligible to produce abridged accounts.

Abridged accounts enable the company to present a simpler balance sheet and profit and loss account, with fewer individual line items (and therefore less detail) – although they must continue to present a ‘true and fair’ view. The company can decide to abridge either the balance sheet or the profit and loss account, or both, but to do so the directors must obtain approval from every shareholder, every year. If the directors do decide to prepare abridged accounts, then these are the accounts that will be delivered to the company’s members and also filed for the public record.

Abridged accounts must include the following elements:

- Abridged balance sheet and/or abridged profit and loss account.

- Director’s signature and printed name on balance sheet.

- Auditors’ report (unless claiming exemption).

- Directors’ report – including signature and printed name of a director or secretary. A strategic report and/or business review is not required.

- Notes to the accounts.

- Statement on the balance sheet above the director’s signature that the accounts have been prepared in accordance with the provisions of the small companies’ regime.

- Statement that all members agreed to the abridgement.

When fully implemented the Economic Crime and Corporate Transparency Act 2023 (ECCT Act) will remove the option to file abridged accounts

Accounts for members versus accounts for filing

Before the introduction of The Companies, Partnership and Groups (Accounts and Reports) Regulations 2015, small companies usually prepared full accounts for their members and then often decided to abbreviate the accounts delivered to Companies House – reducing the amount of company data available to view on the public record. However, the amended regulations introduced a ‘file what you prepare’ model, requiring as a starting point that small companies file on the public record the same accounts they have prepared for members.

This amended approach removed the option to file abbreviated accounts. However, it currently remains possible for small companies and micro-entities to file ‘filleted’ accounts, significantly reducing the amount of company detail available on the public record.

‘Filleted’ accounts – small companies and micro-entities

The term ‘filleted’ accounts refers to exemptions that are available under section 444 of the Companies Act 2006. If a company is considered small (or a micro-entity), then regardless of whether it has prepared full or abridged accounts for members, it may elect to ‘fillet’ the accounts it files with Companies House – choosing not to file the:

- profit and loss account, and any supporting notes; and/or

- the directors’ report; and

- if the company has had an audit, and they have decided to exclude the profit and loss account, they can also choose to remove the auditors’ report – although they may have to include some details regarding the audit in the balance sheet notes.

Note the distinction here. It means that small companies can currently decide to provide more detail for their members than they disclose to the public.

Ready to file micro-entity accounts?

Inform Direct provides a simple and efficient approach to the task of producing fully compliant micro-entity accounts for private companies limited by shares or guarantee.

The ability to ‘fillet’ accounts filed for the public record means that:

- Micro-entities – currently need only file a balance sheet with footnotes. The balance sheet must include a statement that the profit and loss account has not been filed and that the annual accounts are delivered in accordance with the small companies’ regime.

- Small companies – can currently choose to prepare accounts for the members that include a full profit and loss account and an abridged balance sheet. The filed accounts could then be ‘filleted’ – removing the profit and loss account and directors’ report. This significantly reduces the amount of detail filed on the public record (and therefore available to competitors), but every member of the company must authorise this approach, every year.

When it is fully implemented the ECCT Act will remove the option to file ‘filleted’ accounts.

Dormant company accounts

Section 1169 of the Companies Act 2006 states that a company is dormant if it has had ‘no significant accounting transactions’ during an accounting period. In fact, there are only a few, very specific transactions that a company may put through their accounts and still be considered dormant, and these are explained in our article ‘What is a dormant company?’

Having established that dormant status may apply, the next question to consider is whether the company has always been dormant from the moment of incorporation. For the simplest dormant companies that have never traded, a significantly abridged dormant accounts template has been produced by Companies House (Form AA02 (DCA)) and it takes a matter of moments to software file this using Inform Direct.

Need to file dormant company accounts?

Your dormant company still needs to file accounts, but Inform Direct makes it a really simple process.

Read moreIf the dormant company has previously traded, Form AA02 (DCA) is not available. However, unaudited dormant company accounts may be filed with Companies House. These are very simple and comprise:

- A balance sheet including the director’s signature and printed name.

- Statements above the director’s signature to the effect that the company has been dormant throughout the year, together with statements required if the company is claiming audit exemption and if the accounts have been prepared in accordance with the provisions of the small companies’ regime.

- Any previous year’s figures for comparison.

- Certain prescribed notes to the balance sheet.

Whatever type of company accounts you are filing, you can use our simple one-step process to produce prepopulated board minutes recording the directors approval of the accounts – even when the company accounts were not created or filed using Inform Direct.

The ECCT Act will introduce changes to the accounts filing options available to small companies

The Economic Crime and Corporate Transparency Act 2023 (ECCT Act) will introduce changes to the company accounts filing options available to both small companies and micro-entities. The timeline for introduction of the changes is not yet clear as they will be implemented through secondary legislation. However, once fully implemented The ECCT Act will mean that:

- The option to prepare and file abridged accounts will be removed.

- Companies will be required to prepare accounts that comply with s396 of the Companies Act 2006. This means that both small companies and micro-entities will be required to file their profit and loss account.

- Small companies will be required to file a directors’ report (although micro-entities will continue to choose whether they prepare and file a directors’ report).

- Even though the profit and loss account must be filed, the Registrar will have the discretion not to make it publicly available for small companies and micro-entities, perhaps if it discloses commercially sensitive information.

- Companies claiming audit exemption must provide an enhanced statement on the balance sheet, detailing the exemption applied and confirming eligibility.

Preparing statutory accounts is more straightforward if your company records are up to date. Inform Direct is the perfect tool to help you easily keep everything up to date.

A previous version of this article was originally published on 26 July 2018. It was fully updated on 28 May 2025.

Thanks for the details. Is it possible to let us know what type of information, do we need to submit in the “Notes to accounts” ?

Thank you for your question. Briefly, the main aim of the notes to the accounts is to provide enough detail to enable the reader to understand what they are reading. They outline the principal accounting policies applied (i.e. the standards that have been followed when preparing the accounts and details of how the amounts have been reached) as well as providing a breakdown of some of the key figures. For example, there will be notes to explain how assets are valued and when income is recognised. Other notes will provide further analysis of key figures on the balance sheet and profit and loss. For example, a note to the accounts will breakdown the one amount shown for ‘Tangible Assets’ to show how much relates to freehold property, plant and machinery, motor vehicles, computers, etc. Many notes to the accounts are required by law and are set out in various accounting standards. In general, the smaller the company, the fewer notes will be required. When you are preparing a set of financial statements it is essential that you check thoroughly to confirm that you have included all the correct notes and presented them in a compliant format.