Following the coronavirus outbreak and with many businesses no longer able to trade, the Government launched the coronavirus job retention scheme (CJRS) which introduced provisions for companies to furlough employees. This guide looks at furloughing with particular focus on directors, and is supported by free templates to compliantly document the furlough of a director.

Under the CJRS, employers will be able to claim for government grants up to the lower amount of:

- 80% of an employee’s regular salary (plus the associated employer National Insurance contributions and minimum automatic enrolment employer pension contributions on that salary); or

- £2,500 per month.

However, what was not clear, at least when the CJRS was first announced, was whether businesses could furlough directors.

This is because a key element of being furloughed was the strict requirement to do “no work” whereas one of the statutory duties of a company director is “to promote the success of the company“. Clearly the concurrent requirements to do “no work” and “to promote the success of the company” conflict with each other.

Easily manage officer records

Inform Direct is the easy way for companies to manage officer records.

> Easy online forms to appoint and terminate

> Keep all officer details correct and up to date

> Print compliant board minutes and resolutions

> Huge range of other compliant templates

> Automated updates to statutory registers

> Officers synchronised with Companies House

HMRC addressed this issue on 4th April and advised that firms could furlough directors. In particular HMRC said:

Company directors owe duties to their company which are set out in the Companies Act 2006. Where a company (acting through its board of directors) considers that it is in compliance with the statutory duties of one or more of its individual salaried directors, the board can decide that such directors should be furloughed. Where one or more individual directors’ furlough is so decided by the board, this should be formally adopted as a decision of the company, noted in the company records and communicated in writing to the director(s) concerned.

Where furloughed directors need to carry out particular duties to fulfil the statutory obligations they owe to their company, they may do so provided they do no more than would reasonably be judged necessary for that purpose, for instance, they should not do work of a kind they would carry out in normal circumstances to generate commercial revenue or provides services to or on behalf of their company.

This article sets out the four steps that we believe a business should take to furlough one or more executive directors in accordance with the HMRC statement. The CJRS scheme is not applicable to non-executive directors. It is also worth noting that it is much more straightforward to meet the requirements of the CJRS for a company with two or more directors than for a company with just one director.

1 The board of directors must conclude that the best way "to promote the success of the company" is to furlough one or more directors

The decision to furlough one or more directors of the company should be made by the board of directors. Accordingly, to achieve that a board meeting could be convened. The procedure for doing this, and any restrictions on holding a meeting remotely, will be set out in the articles of association of the company. In short, each director must be given notice of the meeting and the nature of the business to discuss.

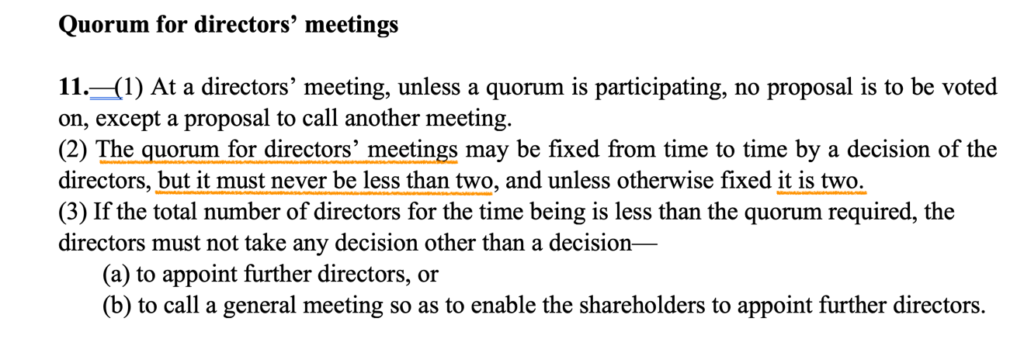

At the board meeting it is important to establish that the meeting is quorate i.e. enough directors are in attendance to pass a resolution. The number of directors needed to make a meeting quorate will be set out in the articles of association. If a private company limited by shares has adopted the model articles without amendment then clause 11(2) – reproduced below – states that to be quorate there should be two directors.

Companies with just one director, which adopted the model articles without amendment, will not need two directors to be quorate, by virtue of clause 7. However, companies with two or more directors should consider revising clause 11.2, if they will struggle to make their meetings quorate. We provide an alternative to the model articles which, alongside other possible enhancements, provides for a board meeting to be quorate with only one director and have written a guide explaining how to change the existing articles of association in whole or in part.

2 The decision to furlough one or more directors must be formally minuted

We have prepared a template board minute recording the decision to furlough one or more directors. You will need to amend the minute to fit your particular circumstances and, if relevant, include any other decisions made at the board meeting.

Companies that fail to minute a decision to furlough one or more directors will be at risk of HMRC subsequently challenging the grant.

3 The decision to furlough one or more directors must be communicated in writing to the director(s) concerned

This is an important step. Not only is it a change to their contract of employment but it is explicitly required by the HMRC guidance. We have prepared a template letter you can use. In the letter the company should set out:

- That the company is designating the director as furloughed;

- The pay the director will receive while furloughed; and

- How long the period of furlough will last

With regard to pay, only the PAYE salary element is covered by CJRS. Dividends do not qualify.

4 The director(s) being furloughed should consent

The director being furloughed should agree to the provisions in the letter from the company and it is appropriate for that agreement to be documented. The draft letter detailed in Step 3 above includes a pro forma acceptance letter for the director being furloughed to sign.

As well as accepting the change to their terms of employment it is prudent to ask for an undertaking to repay any money which HMRC may decide to reclaim from the company in connection with the CJRS if they determine that the original claim was not justified, particularly if it is invalidated by the actions of the employee. Accordingly, the pro forma letter includes such a provision.

Note that in the case of a company furloughing the sole director the individual will sign the letter from the company to the individual director in their company capacity and the letter as a director to the company accepting the terms of being furloughed in their individual capacity.

What happens next?

The furloughed director(s), who must have been on the payroll on or before 19 March 2020 (previously 28 February 2020) and which were notified to HMRC on an RTI submission on or before 19 March 2020 must cease all work immediately, but they can do what is required to fulfil any statutory obligations.

If there were two or more directors and at least one has not been furloughed then HMRC (who will be implementing and policing the CJRS) might expect the still working director to carry out all the statutory obligations alongside their other work and the furloughed director(s) to genuinely do ‘no work’. However, if all the directors are furloughed (or if there is only one director and they furlough themselves) then what are the statutory obligations which can be undertaken without infringing the ‘no work’ stipulation?

What are the statutory obligations?

The statutory obligations are defined in the regulations as meaning complying with an Act of Parliament (e.g. Companies Act 2006) in relation to filing the company’s accounts or provision of other information relating to the administration of the director’s company.

So while the definition is quite narrowly drawn it is generally accepted that the following activities would qualify as statutory obligations:

- Filing VAT, PAYE and Corporation Tax returns

- Filing accounts

- Maintaining the statutory books

- Updating Companies House

- Paying staff/making the claim for the CJRS

- Health & Safety or environmental requirements

Equally, it must be that a director who has been furloughed should not undertake any of the below:

- Trading

- Marketing or business planning

- Client meetings

- Refurbishing the office

Areas which are important to the company, but which might not necessarily be considered statutory obligations, include:

- Bookkeeping, credit control and banking

- Dealing with post and emails

- Paying suppliers/utilities

- Resolving rent negotiations with landlords

- Renewing insurance cover

Provided the director has acted reasonably – particularly when it is a company with only one director – it is hoped that HMRC will take a benign approach to directors attending to the above activities and that claims under the CJRS will not be jeopardised.

That said, it is incumbent on sole directors who have furloughed themselves to do no more than the absolute minimum to maintain their company. Otherwise, they risk the double calamity of their claim under the CJRS being rejected and the business being imperilled.

Take advice if you are unsure what to do

Until March this year very few of us had ever heard of the term furlough. A lot of new provisions have been implemented in a very short space of time and the rules and their interpretation continue to develop. This article is based on our own understanding of the position as at the stated date of publication. If you are at all unsure about these rules, how they affect you or your business and what to do in response, we would strongly encourage you to take professional advice from your accountant or solicitor.