A Person with Significant Control (PSC) is an individual who exercises a significant level of influence or control over a company. It is a legal term designed to enhance transparency and accountability in corporate governance by identifying key people in companies.

The concept of PSC was introduced as part of the Small Business, Enterprise and Employment Act 2015. Companies are required to identify their PSCs and provide this information to Companies House. Failure to do so can result in penalties.

It is also possible for a corporate entity, rather than an individual, to exert significant influence or control. This is covered in a separate article on RLEs (relevant legal entities).

Inform Direct makes it easy to keep track of your PSCs

Inform Direct guides you through recording PSC details and submits PSC statements to Companies House that are compliant with the prescribed wording required by legislation, keeping your company's PSC records up to date.

In this article we look at what makes someone a PSC and what information about them needs to be sent to Companies House.

A PSC is by definition an individual person who meets one or more of the following conditions:

- They hold more than 25% of the company’s shares

- They hold more than 25% of the company’s voting rights

- They have the power to appoint or remove a majority of the company’s board

- They have the right to exercise or actually exercise significant influence or control over the company

- They have the right to exercise or actually exercise significant influence or control over a trust or a firm that is not a legal entity which itself satisfies any of the first four conditions.

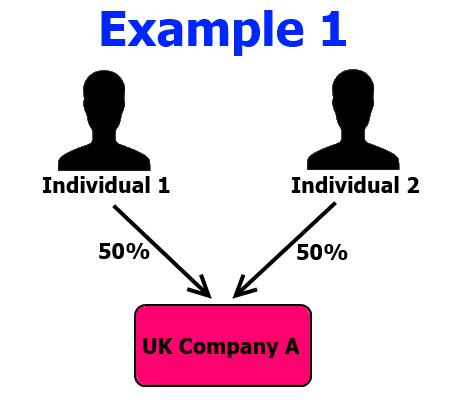

In Example 1, Company A has two shareholders, each holding 50% of the shares.

Because they each hold more than 25% of the company’s shares, both Individual 1 and Individual 2 will be entered on the PSC Register. Assuming all the shares carry one vote, they will also both be noted in the register as holding more than 25% of the company’s voting rights.

Unless there is someone else who has special rights to appoint or remove a majority of the board, or exerts “significant influence or control”, Individuals 1 and 2 will be the company’s only PSCs.

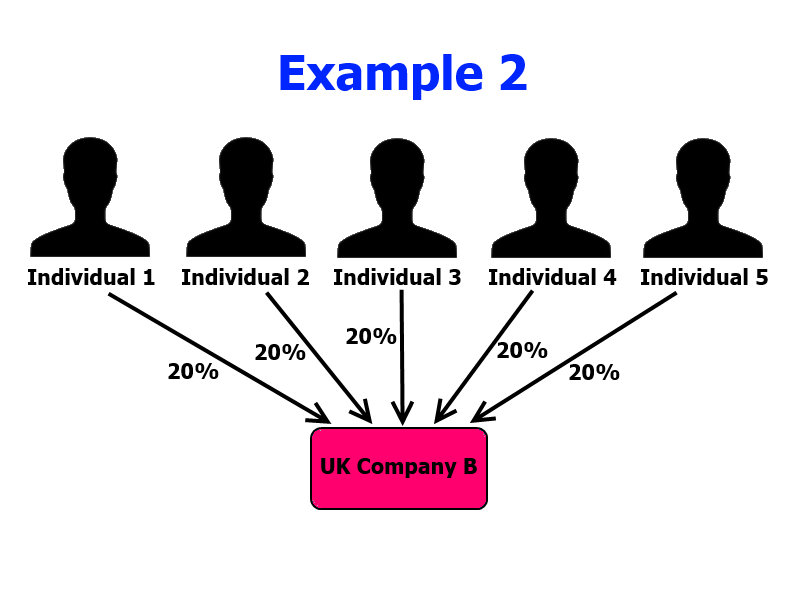

In Example 2, Company B has five shareholders, each with 20% of the company’s shares.

Because no single shareholder holds more than 25% of the shares (or voting rights), none of these individuals will be entered on the PSC register.

Assuming there’s no one else who meets any of the conditions, Company B doesn’t have any PSCs. That’s perfectly acceptable, but the fact there are no PSCs must itself be entered on the PSC register. The PSC register can never be blank.

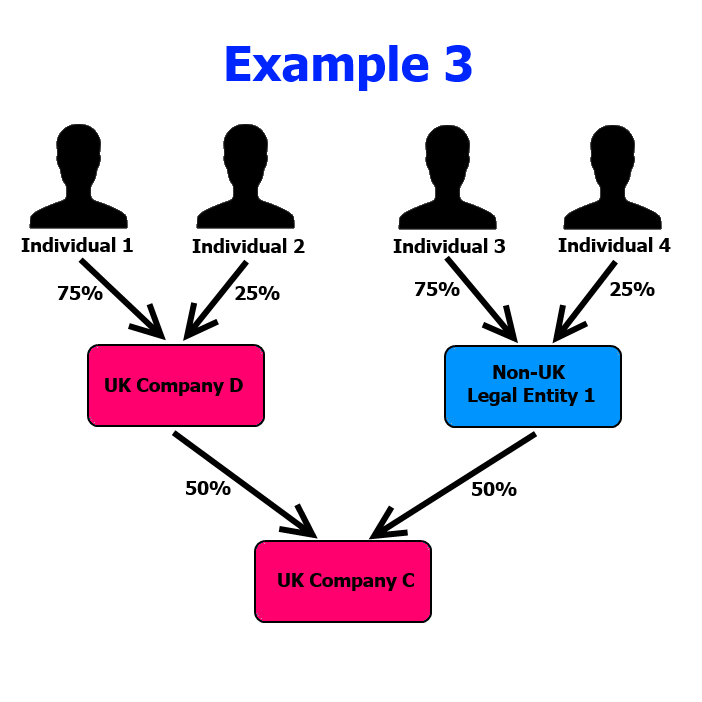

An individual can meet several of the conditions – e.g. shareholding and voting rights – directly or indirectly. Examples 3 and 4 cover indirect ownership scenarios where shares and voting rights are held indirectly via an ownership chain.

Usually, where a corporate entity holds shares in a UK company and, had it been an individual, would have met one or more of the control reasons, that company would be classed as a relevant legal entity (RLE) and appear on the PSC register. So RLEs can be described as ‘corporate PSCs’.

So UK Company D will appear on the PSC register of UK Company C as it holds 50% of the shares and voting rights. Because Company D is already listed on the register, neither Individual 1 nor Individual 2 appear on Company C’s PSC register.

However, it’s different where a controlling company is not a relevant legal entity – for example, it’s based in Barbados.

Because it’s not classed as a relevant legal entity, Non-UK Legal Entity 1 cannot appear on Company C’s PSC register. Instead, we have to look back and see if anyone has a majority stake in Non-UK Legal Entity 1. In this case, Individual 3 has a majority stake because he controls more than 50% of the voting rights. Therefore, it’s Individual 3 who must appear in Company C’s PSC register, alongside UK Company D.

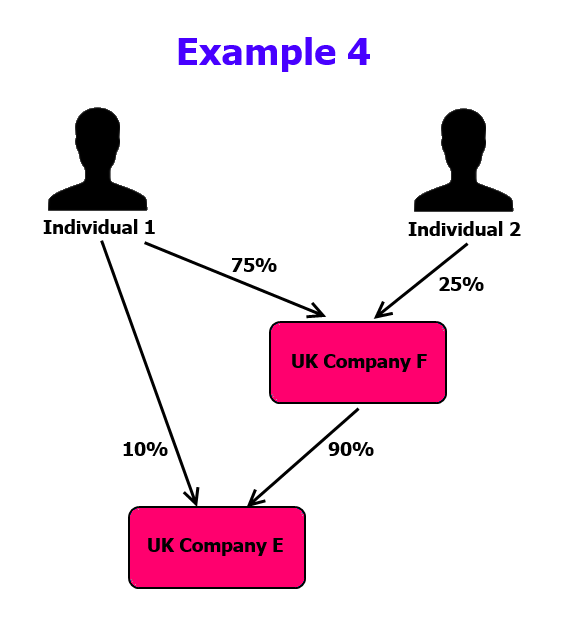

Example 4 illustrates another oddity of indirect ownership.

If Individual 1 only held shares directly in UK Company E, they wouldn’t need to be on its PSC register (because the holding is not more than 25%). If they only held an interest indirectly via UK Company F, it would only be F rather than also Individual 1 who would appear on E’s PSC register.

But because they hold shares both directly and as an indirect holding via a majority stake in F, Companies House require that Individual 1 is shown on the PSC register of UK Company E.

UK Company F would also appear on E’s PSC register.

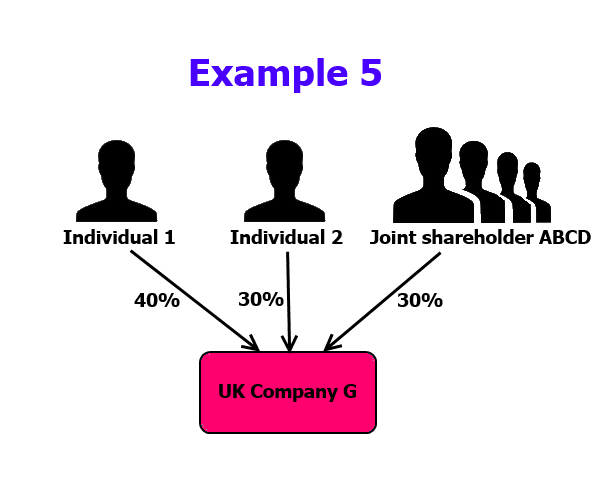

A joint shareholding is not counted singly for the purposes of the PSC register. Instead, every joint shareholder is treated as if they each hold the total number of shares or rights that are held jointly.

In Example 5, because the joint shareholding exceeds 25% of the shares and voting rights, each of the joint shareholders A, B, C and D who hold the shares jointly must appear on UK Company G’s PSC register (alongside Individuals 1 and 2). That’s despite the fact that, unlike the individual shareholders, they share the rights between them.

While it’s counter-intuitive for Company G’s PSC register to show six individuals each holding more than 25% of the shares and voting rights, that’s what the legislation requires.

What information about an individual PSC goes in the register?

For an individual PSC, the register must contain the person’s:

- Name

- Service address

- Nationality

- Country of residence

- Date of birth

- Usual residential address

- The date on which the individual became registrable

- The nature of their control over the company – which of the conditions above the individual meets and, for shareholdings and voting rights, which of a number of discrete bandings they fall into

- Any restrictions on disclosure of the PSC’s information that are effective.

Before the individual’s name and other details can be entered into the register, it must have been confirmed. Until then, the company must put a specially worded statement in the register that a PSC has been identified but that their details are not yet confirmed. Information is confirmed when:

- The PSC supplies the company with the information

- The information is supplied to the company with the knowledge of the PSC

- The company asks the PSC to confirm that listed information is correct and the individual says it is

- The company holds information that has previously been confirmed and has no reason to believe it has since changed.

The 2023 Economic Crime and Corporate Transparency Act (ECCTA) removes the requirement for companies to keep ‘local’ PSC registers. Once the relevant part of ECCTA comes into force, it will no longer be a legal requirement to keep a local PSC register at the company’s registered office address or single alternative inspection location (SAIL). The only official PSC register will be the central one kept at Companies House.

Many companies will find it useful to continue to maintain their local PSC register as it provides an independent reference that can be printed off and consulted at any time and is good record-keeping practice.

Inform Direct has full functionality to maintain both local and central PSC registers. It allows you to keep a record of the progress of PSC investigations in Inform Direct and produces a local register. It also submits the required information to Companies House on the correct forms to be stored on the central PSC register, keeping PSC information up to date for the company.

Manage company records easily in Inform Direct: dedicated company secretarial software that saves time and keeps everything organised.

These examples are all well and good, but what about Directors in RTM companies ? They usually exercise direct influence over a Company.

EXACTLY I was looking these answers. very good explanation.

Thank you