This is an introduction to classifying items in the assets section of the balance sheet for a micro-entity, the smallest type of company. It’s a good place to start because it’s one of the simplest forms of company accounts, and many of the basic principles about assets also apply to other sizes of company.

How are assets organised on the balance sheet?

To build a balance sheet we need to take assets and organise them into categories. This article gives some guidance on how to achieve this by listing some of the most common categories in typical micro-entity balance sheets. Let’s begin with a universal distinction:

Fixed vs. current assets

Fixed assets: These are long-term assets held by your business: land, buildings, machinery, fixtures and fittings, computer equipment and vehicles. Fixed assets can also be intangible assets with a long useful life such as copyrights, patents and goodwill.

Streamline your Companies House accounts

Inform Direct makes it easy to:

> Prepare and file fully compliant accounts

> Get it right first time and reduce rejections

> Only file what Companies House needs

> Automate micro-entity & dormant accounts

Current assets: Current assets are short-term assets that can be easily converted into cash within a year. Examples include bank accounts, accounts receivable, debtors, stock, inventory, and prepaid expenses.

Let’s dive deeper into each of these categories to see what they contain.

1. Fixed assets

Fixed assets have value to the business that extends beyond the current accounting period. They are not expected to be converted into cash within a year but have ongoing value to the business. The following asset types fall under fixed assets but are not always broken out separately. They are often condensed into a single line item, ‘fixed assets’.

Tangible assets

Tangible fixed assets are physical items that represent a significant investment for the company and underpin its operations in the long term. They include equipment, buildings, furniture, computers and vehicles that the company uses regularly and plans to use over time. They come under tangible assets on the balance sheet as initial value less depreciation.

Accounting for depreciation of tangible assets

Here we describe a simple method (the straight line method) of calculating depreciation of tangible assets that is suitable for micro-entity accounts.

- Find out the future scrap value of the asset when it will have reached the end of its useful life.

- Subtract the scrap value from the initial cost of acquiring the asset.

- Divide this figure by the number of years the asset is expected to be of value to the company.

- Write down this annual cost as an expense each year on the income statement (profit and loss account).

- Put the remaining value of the asset on the balance sheet.

In this way depreciation is treated as an expense and gradually transferred from the balance sheet to the income statement (profit and loss account).

Investments

If your business has investments such as stocks and shares in other companies that extend beyond the current accounting year, create a separate section to account for them. Include the cost of acquisition and any changes in value since the initial investment.

Intangible assets

Intangible fixed assets are non-physical but can have great value to the company. They can include trademarks, copyrights, patents, brands, intellectual property, customer lists and goodwill.

Intangible assets are treated differently according to whether they were acquired by the company or created internally. Those it has acquired are listed as assets on the balance sheet, but those it generates internally are not. Instead, any expenses incurred by creating them are entered as expenses on the income statement. So in fact patents, brands, trademarks, intellectual property and such, if internally generated, have no place on the balance sheet for micro-entity companies. In other words, they cannot be capitalised. This can mean that a company’s most valuable assets do not appear on its balance sheet.

Goodwill

If your company has acquired any other businesses or their brands and trademarks, it may be necessary to account for the goodwill associated with them on your company’s balance sheet. Goodwill represents intangible assets like reputation and brand value. It generally arises from acquisitions where the acquiring company has paid a premium over and above the value of the net assets. In the UK, goodwill is usually amortised (written off in annual instalments) over up to ten years. Goodwill generated within your own company is only recognised when your business is sold.

2. Current assets

Current assets are short-term assets that are easily convertible into cash or may be used up during the current accounting year. They are vital for day-to-day operations and liquidity. The following are common categories for current assets as they appear on the balance sheet.

Called up share capital not paid

This is the nominal value of any shares the company has issued but for which it has not yet been paid. It is treated as a current asset because the money is owed to the company.

Paid-up share capital (the value of shares that have been paid for) comes under equity (capital and reserves) on the balance sheet.

Stock

Stock is finished goods manufactured or purchased ready for sale, but not yet sold. Inventory, in contrast, also includes raw materials and unfinished products. Stock only applies to companies that sell physical products.

Debtors: amounts falling due within one year

This is money owed to the company by customers who have bought its products and services but not yet paid for them. There are many reasons for this. One example could be that the customer is on 90-day invoicing terms with the company.

The debtors section also includes any other amounts owed to the company, for example director’s loans, tax rebates from HMRC and loans to other companies.

Prepayments and accrued income

Prepayments and accrued income are adjustments made by some accountants in order to present a true and fair account of the company’s finances. Both are recorded as current assets.

- Prepayment: A payment made to the company during a prior accounting period which is incurred in the current period. One example might be a software licence that lasts two years and was paid for in full last year.

- Accrued income: An amount not yet invoiced but expected to be received during the current accounting period, even though it was initially incurred in the previous An example might be a consulting fee spanning two accounting periods and payable in full at the end.

Cash at bank and in hand

- Positive bank balance at the date of the balance sheet. Any overdraft should be put under current liabilities.

- ‘In hand’ is actual notes and coins held by the company that are not in the bank. It might include the contents of the cash register or petty cash.

How to calculate net assets

Add together all the fixed and current assets you have identified. Then subtract your liabilities. This gives a figure known as ‘Capital and Reserves’ at the bottom of the balance sheet. It indicates the total ownership interest and accumulated profits of the shareholders in the company. It’s an important indicator of the financial health and stability of the company.

Further understanding asset types

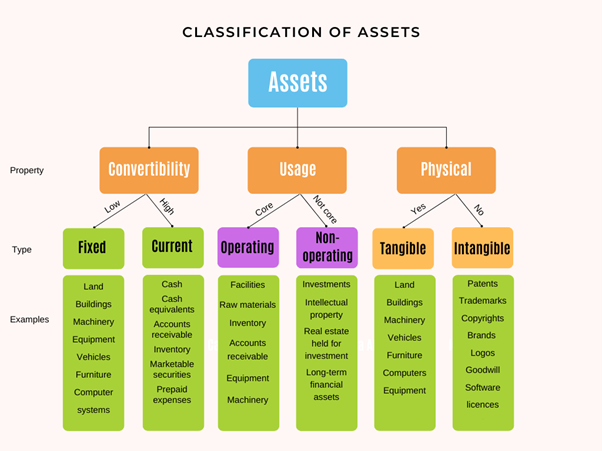

The above is how items are usually laid out on the balance sheet. But there are other ways of thinking about assets. We have seen fixed vs. current and tangible vs. intangible assets. It is sometimes helpful to be aware of another pair of categories:

Operating vs. non-operating assets

- Operating assets: those involved in the company’s core operations. They are indispensable for producing the company’s main product or service. Examples include equipment, machinery and production worker wages.

- Non-operating assets: other assets not related to its core operations. They bolster the company’s bottom line but could theoretically be removed without jeopardising core operations. Examples include investments and other long-term financial assets, unused buildings and unallocated or ‘idle’ cash.

Consider the following chart. There is a degree of overlap between the categories. This is because we are looking at the same assets from three different viewpoints:

- Convertibility: How readily they can be converted into cash (fixed/current)

- Usage: What they are used for: core operations or non-core (operating/non-operating)

- Physical: Whether they physically exist or not (tangible/intangible).

File company accounts on time and keep statutory books up to date simply and easily with Inform Direct.