This article explains what a holding company is and what the reasons are for using one.

A holding company exists to own shares in other companies. It does not do any trading itself but focuses on holding and managing a controlling stake in one or more ‘subsidiary’ companies. It is not directly involved in managing the companies in which it holds stock, but can exercise control by virtue of its majority shareholding. A holding company is an example of a corporate shareholder.

Examples of large holding companies include Unilever, Johnson & Johnson, Virgin Group and Berkshire Hathaway. But far smaller groups exist; holding companies are defined by their structure and purpose rather than their size.

Companies in which the holding company has a controlling stake are subsidiaries. A cluster of subsidiaries is a group. This article outlines the holding company/subsidiaries/group corporate structure.

Holding companies are usually private companies limited by shares. In legal terms their internal structure is no different from that of other limited-by-shares companies. However, they do not exist to trade in goods or services. They exist to own the group’s assets while controlling the subsidiaries.

Group assets can be fixed and financial: land, property, vehicles, furniture, computers, cash, bank deposits, stocks, and so on. However, they can also be intangible assets. This includes intellectual property like copyrights, trademarks and patents. Song rights, for example, are lucrative assets for some holding companies.

Holding companies are designed for building long-term resilience by controlling risk. In a well-managed group of companies the risk is spread throughout the group. One could compare it to a submarine divided into compartments with various functions but which can each be sealed off if necessary to prevent the whole vessel from sinking. The ‘watertight seal’ of limited liability prevents an adverse event that affects one compartment (subsidiary) from taking down the whole crew (members of the holding company).

Holding companies are designed for building long-term resilience by controlling risk.

The relationship between holding company and subsidiary

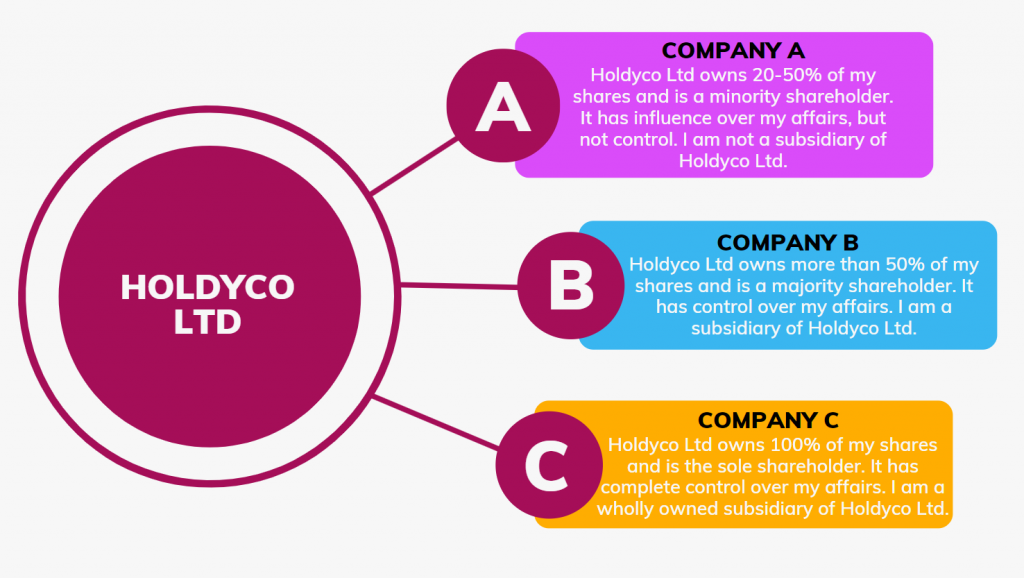

Companies Act 2006, s.1159(1) defines four ways in which the relationship of holding company and subsidiary may arise.

- The holding company has a majority (over 50%) of the voting rights in the subsidiary

- It is a member of the subsidiary and has the right to appoint and remove a majority of its directors

- It is a member of the subsidiary and has agreements in place with other shareholders that effectively give it majority voting rights in the subsidiary

- The company in question is a subsidiary of a subsidiary.

A company becomes a wholly owned subsidiary when a holding company has acquired all of its shares. A wholly owned subsidiary has no obligations to minority shareholders since it is entirely owned by its holding company. The holding company has all the voting rights and thus can exercise complete strategic control over the subsidiary.

Some holding companies’ only activity is receiving dividends from subsidiaries. Others may, in addition to this, actively manage one or more subsidiaries. This can affect the holding company’s tax obligations (VAT on taxable supplies) and its classification (SIC code) at Companies House. See below for more on these.

Form and administer holding companies and subsidiaries

• Comprehensive features for company secretarial tasks.

• Process-driven software ensures accuracy and completeness.

• Amazingly low cost per company (ask us and find out)

A wholly owned subsidiary has no obligations to minority shareholders since it is entirely owned by its holding company.

Is the UK a good place to form a holding company?

The UK is an excellent place to form a holding company. It has extensive historic tax treaties with other nations which mean that many of the tax advantages described in this article apply internationally as well as domestically. These long-standing agreements have not been affected by Brexit.

Advantages of a holding company structure

Risk management

The overall group structure offers an enhanced degree of limited liability in that subsidiaries can serve precise purposes. For example, valuable assets can be held by a non-trading subsidiary, or a high-risk operation may be confined to a subsidiary with no other activities. In a well-run group structure, risk can be managed within multiple silos.

As it is a separate entity, the holding company is protected from liability for a subsidiary’s losses, debts or legal failings. This includes wholly owned subsidiaries. However, there are occasionally circumstances in which a holding company may find itself liable for a subsidiary’s debts, so professional legal advice should be taken at all stages.

Asset protection

A well-structured group’s assets are owned by the holding company rather than the trading subsidiaries, which are more vulnerable to business risks. Often the holding company will lease the assets to its subsidiaries. The idea is to protect the shareholders rather than allowing assets out into the wild where they could ultimately be sold off in the event of a subsidiary becoming insolvent.

Tax advantages of a holding company

In addition to enhanced risk management, holding companies benefit from significant tax advantages. The following are some of the main tax breaks for holding companies.

Tax-free dividend payments

Subsidiaries can pay dividends to the holding company without creating a corporation tax liability. This exemption simplifies tax planning and profit extraction by the shareholders of the holding company.

Subsidiaries can pay dividends to the holding company without creating a corporation tax liability.

Stamp duty exemptions

Generally property can be moved around within the group without stamp duty being payable.

The substantial shareholding exemption (SSE)

The substantial shareholding exemption (SSE) exempts a holding company from capital gains tax on disposal of its shares in a subsidiary.

The general rule is that a company holding over 10% of the shares in another company for a period of 12 months during a 6-year period preceding the disposal pays no tax on gains arising from the disposal of those shares. This is on the condition that the subsidiary has been an active business for 12 months before the disposal.

These rules were revised in April 2017. Previously it was a 2-year rather than 6-year period and both holding company and subsidiary had to have been an active business for 12 months prior to the disposal. More details of the 2017 SSE reform can be found on the government website here: Reform of Substantial Shareholding Exemption for qualifying institutional investors.

The substantial shareholding exemption places many holding companies in a favourable tax position as regards the flow of funds from their subsidiaries. That being said, this can be a complex area and professional tax advice should always be sought when considering the use of a holding company.

The substantial shareholding exemption (SSE) exempts a holding company from capital gains tax on disposal of its shares in a subsidiary.

VAT exemption and taxable supplies

If a holding company’s only functions are to acquire and dispose of shares, receive dividend payments and protect assets, the government does not view these functions as taxable supplies. The holding company is therefore not liable for VAT. However, if the holding company provides services to a subsidiary such as management services, these are taxable supplies. Therefore, VAT is payable when the annual taxable turnover exceeds £85,000 (correct for the 2020-2021 tax year).

Tax-neutral transfer of assets between group companies

The Taxation of Chargeable Gains Act 1992 s. 171 provides that a group of companies can move its assets around between companies without immediate capital gains consequences. CGT will only be payable when the asset is disposed of outside the group. This is known as the ‘no gain/no loss rule’.

The HMRC capital gains tax manual says of the no gain/no loss rule ‘… it recognises that business activities carried on within the overall economic ownership of a corporate group, within the charge to corporation tax, should, in broad terms, be tax neutral.’ In other words, for CGT purposes it treats a group of companies as a single economic entity.

Overseas tax advantages

To reduce the corporate tax payable, the holding company can be set up in a tax-friendly overseas country. This is often referred to as an offshore holding company.

Seek professional tax advice

We strongly recommend seeking professional tax advice when setting up a group company structure. Planning is essential for reasons including:

The tax implications may be different depending on whether a holding company is created at outset or later formed and inserted into a group structure. In the latter scenario, care is needed to avoid tax charges on movements of assets.

There are disposal issues to consider when you decide to sell a company in the group. These include changes made in the Finance Act 2020 to stamp duty on the sale of shares in a group company. This has closed down a popular tax avoidance technique known as swamping which involved a share reorganisation designed to minimise the taxable value of shares being disposed of.

Finance

A holding company structure can offer more flexibility in credit and borrowing. Finance can be tailored by approaching different lenders and negotiating different credit terms to suit the needs of each company in the group.

Certain rules exist on loans to directors for most limited companies, such as the requirement for shareholder approval for any such loan. However, this rule does not apply when the loan is to a director of a wholly owned subsidiary.

This is a complex area. We strongly recommend taking professional advice to ensure actions are consistent with the directors’ duty to protect the interests of the company.

Disadvantages of a holding company structure

Downsides of operating a group structure may include:

- More complicated to administer. Each subsidiary must maintain its own accounts and company records. Transactions between group companies need tracking and accounting for.

- Increased legal and accounting costs may offset the tax efficiency gains of a group of companies.

- Possible disagreements between a subsidiary and the holding company leading to management conflict.

- Potential for unethical directors to hide the true position by moving assets etc. around the group.

How to form a holding company

Holding companies are formed via the same process as any other private company limited by shares:

- Establish a registered office address

- Choose a company name and SIC code (see below)

- Name the director(s)

- Name the shareholder(s)

- Name the PSC(s)

- Name the company secretary, if there is to be one

- Draw up the memorandum and articles of association

- Send an application for incorporation to Companies House

- Issue at least one share to each shareholder.

When it comes to the articles of association, it is perfectly possible to use the model articles for a holding company but many firms prefer to use bespoke articles tailored to their particular needs.

If the company is formed using Inform Direct, the purpose-built software guides the user through the process. It ensures that all required information is present and complete before making the electronic submission to Companies House. With all necessary information to hand, an incorporation application can be completed and submitted in one sitting.

What SIC code should a holding company use?

The SIC (Standard Industrial Classification) code is a 5-figure code used at Companies House to classify that company’s core business activity. Holding companies do not trade in goods or services, so what SIC code should they use?

In fact, they are well catered for as there is a range of SIC codes to cover most types of holding company. These include:

- Sector-specific ones like 64205 (Activities of financial services holding companies) and 64203 (Activities of construction holding companies)

- A more general one, 64209 (Activities of other holding companies not elsewhere classified).

- If the holding company is heavily involved in managing its subsidiaries rather than simply drawing dividends from them, it may be best classified under another SIC code such as financial management (70221) or management consulting (70229).

Can I use ‘Holdings’ in the company name?

Short answer: yes.

Fuller answer: Prior to 2015, ‘Holding(s)’ was one of the ‘sensitive words’ subject to special restrictions by Companies House. The list of such words also included ‘International’ and ‘Group’. To use these words as part of its name, a company would have to apply for approval and supply supporting information. But in 2015 some sensitive words were declassified and can now be used to form companies with no pre-approval required. ‘Holding(s)’ is one of those words. On our site you can download the current list of sensitive words after the 2014 revision.

The main problem with the word ‘Holding(s)’ in company names was not that it was likely to mislead the public, as ‘Royal’ or ‘Institute’ might. Rather, it was disregarded when deciding whether a company name was ‘same as’ another. Thus, before the 2015 legislation there was no distinction between the names ABC Empresas Ltd and ABC Empresas Holdings Ltd. Companies House would have viewed them as the same company. This reduced the supply of available company names and led to disputes.

The main problem with the word ‘Holding(s)’ in company names was not that it was likely to mislead the public, as ‘Royal’ or ‘Institute’ might. Rather, the word was entirely disregarded when deciding whether a company name was ‘same as’ another.

Nowadays Companies House takes a more literal approach to company names. The result is that it is much easier to register a company name if another similar-looking one is already registered. Use our company name checker to see if a name you are considering is available.

For more about company names in general and why it is wise to check before you register one, see our article on company names.