How to replace a lost share certificate

Everyone loses things, and shareholders will sometimes lose their share certificates. By lose, we mean anything ranging from damaging or misplacing share certificates right through to having them stolen.…

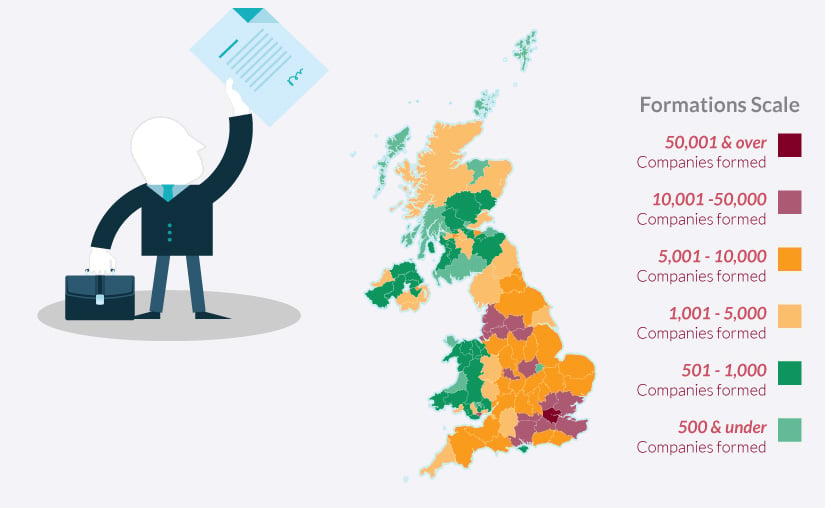

2025 Review

of UK Company Formations

Read our comprehensive review of UK company formations in 2024, year-on-year growth rates and breakdown by county. This detailed insight is provided in the form of easy to understand infographics available for sharing through social media and on your own website