Most small standalone UK companies will qualify for exemption from audit. However, there are additional requirements that you must consider if your company is a member of a group.

How might a UK subsidiary qualify for audit exemption?

There are several potential routes via which a UK subsidiary may qualify for audit exemption:

- Small group company audit exemption: s477 and s479 Companies Act 2006.

- Parent guarantee: s479A Companies Act 2006.

- If the UK subsidiary is dormant: s480 Companies Act 2006.

Unless your UK subsidiary is a dormant company, the most straightforward route, if it is available, is to claim small company audit exemption. However, if either the individual company or the group do not meet the criteria to qualify as small, then the parent guarantee may offer an alternative solution.

Want to make it much easier to manage your UK company?

An important part of managing a UK company is keeping its statutory books and filings up to date. Inform Direct is the perfect tool to help make this task a whole lot easier.

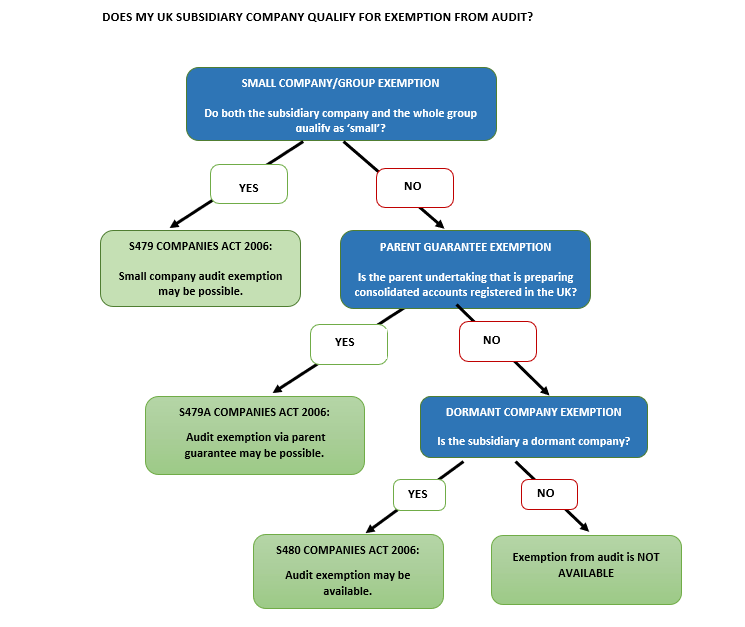

Start nowYou may find it useful to consult the flowchart below, which illustrates the different routes visually:

Flowchart illustrating the different routes to audit exemption for a UK subsidiary company

Let us consider each option in turn, beginning with when small company audit exemption may be available to a UK subsidiary.

Size matters – does the individual company qualify as a ‘small’ company?

When considering whether small company audit exemption may be possible for a group company, you should start by looking at the size of the subsidiary itself. It must qualify as a ‘small’ company in accordance with section 477 of the Companies Act 2006. Our related guide will help you to determine the size of the individual company and whether it may be eligible for small company audit exemption.

Is the group a ‘small’ group?

Having satisfied yourself that the company would qualify for small company audit exemption were it to be considered as a standalone entity, you must now consider how its status as a group company will affect this.

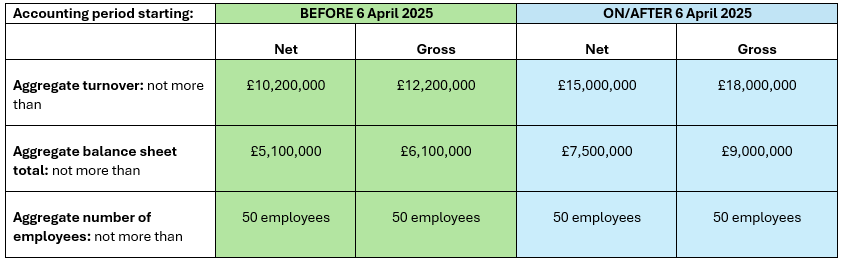

The first step is to consider whether the group of companies would qualify as a ‘small’ group. Section 479 of the Companies Act 2006 allows eligible ‘small’ group companies to apply audit exemption. Section 383 defines the size criteria that qualify a group as small. The thresholds were updated by The Companies (Accounts and Reports) (Amendment and Transitional Provision) Regulations 2024, with the new increased thresholds (shown in the table below) applying for accounting periods starting on or after 6 April 2025. When considering the size thresholds (given below), you must make the calculation based on the largest possible group, considered on a worldwide basis. You can calculate the values on either a net or a gross basis:

Note the following:

- Net: means as per the consolidated accounts (i.e., after any adjustments made to eliminate group transactions).

- Gross: reached by adding together all the individual company accounts before any intragroup transactions or balances are removed.

- The maximum figures quoted in the table above apply where the accounting period is 12 months in length. Where the accounting period in question is not actually a year – the ‘Turnover’ value should be adjusted proportionately.

The group will qualify as ‘small’:

- In the first year of trading: if it can meet at least two out of three of the size criteria.

- In subsequent years: unless it exceeds two of the three size thresholds for two years in a row.

Having determined that the group qualifies as a ‘small’ group, you should next consider its eligibility.

Could the group be ineligible?

Section 479 of the Companies Act 2006 prohibits audit exemption if at any time within the financial period the group contains an ‘ineligible’ company. This renders the whole group ineligible and every UK company in the group will be required to obtain an audit of its accounts.

Section 384 states that a group is ineligible if any of its members is:

- A traded company;

- A body corporate (other than a company) whose shares are admitted to trading on a UK regulated market;

- An e-money issuer, authorised insurance company, banking company, MiFID investment firm or a UCITS management company;

- A person that carries on insurance market activity or a regulated activity under the Financial Services and Markets Act 2000; or

- A scheme funder of a Master Trust scheme.

It is worth noting that where a group contains a PLC, this will only render the group ineligible if the PLC is also a traded company (i.e., it is listed on the London Stock Exchange).

If both your company and the group that it is part of qualify as ‘small’, and no member of the group is considered ineligible, the company may qualify for exemption from audit.

What about UK subsidiaries that do not qualify as small?

Under the requirements of s479A, subsidiaries that are part of a UK group that does not qualify as small are still able to take advantage of audit exemption, provided that:

- All members of the subsidiary company agree to the audit exemption (including holders of preference or non-voting shares);

- The UK parent company guarantees the liabilities of the subsidiary (as per s479C);

- The subsidiary is included in the audited consolidated accounts prepared by the UK parent undertaking;

- The parent undertaking discloses in the notes of the consolidated accounts that the subsidiary is exempt from audit; and

- The directors of the subsidiary deliver to the registrar on or before the date of the accounts all the required documentation.

Note that in order to comply with the last point, all of the following documents must be delivered to Companies House:

- A written notice of the shareholders unanimously agreeing to audit exemption;

- A statement of guarantee by a parent undertaking of the subsidiary company (Form AA06); and

- A copy of the consolidated accounts including the auditor’s report and annual report on those accounts.

Remember however, that even if the subsidiary can satisfy all the above, section 479B of the Companies Act 2006 does not allow audit exemption if at any time the company was an ineligible company.

It is worth noting that the parent company that provides the guarantee does not have to be the ultimate parent. If an intermediate parent undertaking is registered under the law of any part of the UK and will prepare consolidated accounts for filing with Companies House – then audit exemption via parent guarantee may still be available.

Is audit exemption available to dormant subsidiaries?

Section 480 states that dormant subsidiaries will qualify for exemption from audit if they have been dormant since incorporation, or for the whole of the financial period concerned and:

- have been entitled to prepare individual accounts in accordance with the small companies regime (or would have been so entitled but for being a public company or a member of an ineligible group); and

- have not been required to prepare group accounts for that financial period.

Section 479(3) adds that a dormant subsidiary is still entitled to audit exemption, even if the group to which it belongs is considered ineligible.

However, the ability to claim exemption from audit is removed if at any time during the financial period the dormant subsidiary was (per s481):

- a traded company;

- an authorised insurance company, a banking company, an e-money issuer, a MiFID investment firm, a UCITS management company; or

- a company that carries on insurance market activity.

If your subsidiary company is dormant you may wish to refer to our related guide that looks at other exemptions available to dormant subsidiaries.

Audit exemption can be lost

Even if your subsidiary company does qualify for exemption from audit, there are circumstances in which it may still be required to obtain a statutory audit. These include:

- When members of the company require an audit.

- There is a specific requirement in the company’s articles of association.

- When the required statutory statements are not included on the balance sheet.

- When there is a condition included in a shareholders’ agreement, loan arrangement or other contract.

You can find more details on each of these circumstances in a related guide which considers how to qualify for small company audit exemption.

Inform Direct makes it quick and easy to maintain statutory registers, manage company records and submit filings to Companies House at the touch of a button.

Earlier versions of this article were published in May 2013 and May 2022.