A limited company can distribute its profits via dividends to its shareholders. Once you’ve identified that there are sufficient profits to distribute as dividends, you must follow a compliant process to declare and pay a dividend.

Firstly, the directors’ decision to declare a dividend must be recorded in a board minute.

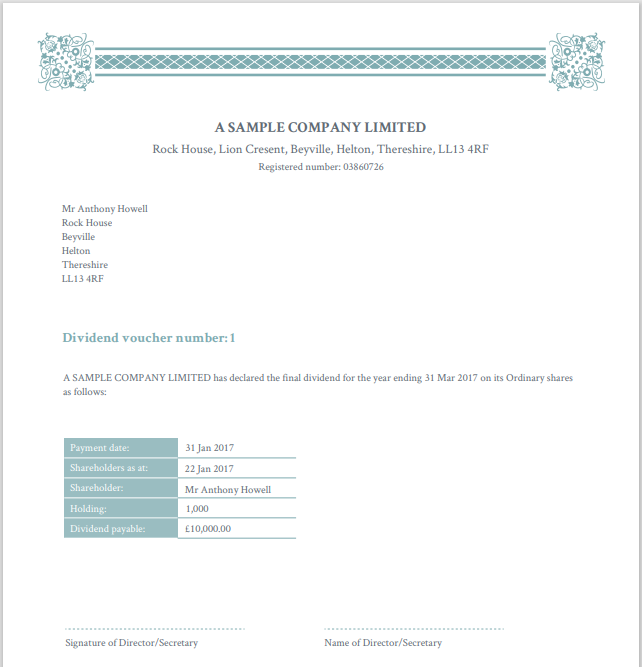

Secondly, the company must issue each shareholder receiving a dividend with a dividend voucher.

The dividend voucher, sometimes also called a dividend counterfoil, acts as a written record – effectively a receipt. It shows who received the dividend and how much it was. A company can either produce the dividend vouchers or ask an accountant to do it for them.

Failure to follow a compliant process may result in penalties from HMRC and it’s important for the company to maintain a record of dividends. Without a proper record of the board’s decision and dividends paid, the dividend may be illegal, or deemed instead by HMRC to be a salary payment. In that case, both income tax and National Insurance Contributions would be due on the payment received.

Easily create dividend vouchers

Inform Direct is the easy way for companies to create dividend vouchers.

> Dividend per shareholder calculated

> Simple process creates all vouchers

> 9 attractive dividend voucher templates

> Compliant board minutes pre-populated

> Full history of dividends maintained

The shareholder receiving a dividend must keep the dividend voucher as evidence for tax purposes. They may need it to complete their self assessment tax return. In another article, we look at how dividends are taxed on shareholders.

The dividend voucher sent to a shareholder must show the following information:

- the company’s name and company number

- the type of security (for example ‘Ordinary shares’)

- the number of shares held by the shareholder

- the date

- the name and address of the shareholder(s) being paid a dividend

- the amount of the dividend paid

- the signature of an officer of the company

Many companies will work from a manual template. However, software like Inform Direct’s dividend voucher creation tool can make creating dividend vouchers a whole lot easier. It takes you through the process of creating dividend vouchers step by step. It also uses shareholder details available from Companies House to save you time. You can create, save and then send professional vouchers including all the right information.

Choose from 9 voucher templates – branded with the company logo if you choose.

Inform Direct also keeps a full record of the dividend vouchers you create. That enables you to meet your obligations and makes it even easier to create the next set of vouchers. That’s particularly useful if a company is paying regular dividends.

Should dividend vouchers be sent by post or electronically?

Dividend vouchers were traditionally always sent to shareholders by post. However, following the Income and Corporation Taxes (Electronic Certificates of Deduction of Tax and Tax Credit) Regulations 2003, dividend vouchers may now be distributed electronically – by email, for example.

Companies and their shareholders might opt for electronic distribution of dividend vouchers because:

- It saves on stationery and postage costs

- Dividend vouchers can be delivered instantly

- It removes the risk of a dividend voucher getting lost in the post

- Electronic communication is more convenient for many shareholders

- Particularly since the onset of the coronavirus pandemic, electronic delivery of documents is increasingly expected by shareholders

Where offered by a company, shareholders will usually need to opt in to receive electronic dividend vouchers. They may choose to withdraw their consent at any time and instead opt to receive paper dividend vouchers again.

What vouchers need to be produced for regular dividends?

Many companies pay dividends more than once a tax year. The standard approach here is still to provide a new dividend voucher each time a dividend is declared.

Sometimes, a company will issue a single summary voucher which covers the whole of the tax year.

What about joint shareholders?

Sometimes a share or shares may be held jointly by two or more joint shareholders.

For a joint shareholder, it’s still good practice to include the name of each separate holder on the dividend voucher. However, only the address of the first named joint holder needs to be shown. You also only need to produce and send a single dividend voucher for a joint shareholding. That voucher will be sent to the first named holder, rather than a dividend voucher to each joint shareholder.

Inform Direct calculates the dividend for each shareholder and produces beautiful dividend vouchers for you to send to them.