Whenever a contractor considers approaching a client or agency for work, they face a dilemma over how best to get paid. UK tax laws tend to push them into choosing between two options:

- Using their own limited company to supply the work and receive payment

- Using an umbrella company as an intermediary employer between themselves and the client.

In this article we examine what umbrella companies are and how they work with contractors and agencies. We will be comparing them with the other option of working via the contractor’s own private limited company.

Quick, simple company records management

Maintain limited company records quickly and easily with dedicated company secretarial software.

Inform Direct tells you which forms you need to submit and when, and guides you step by step.

What is an umbrella company?

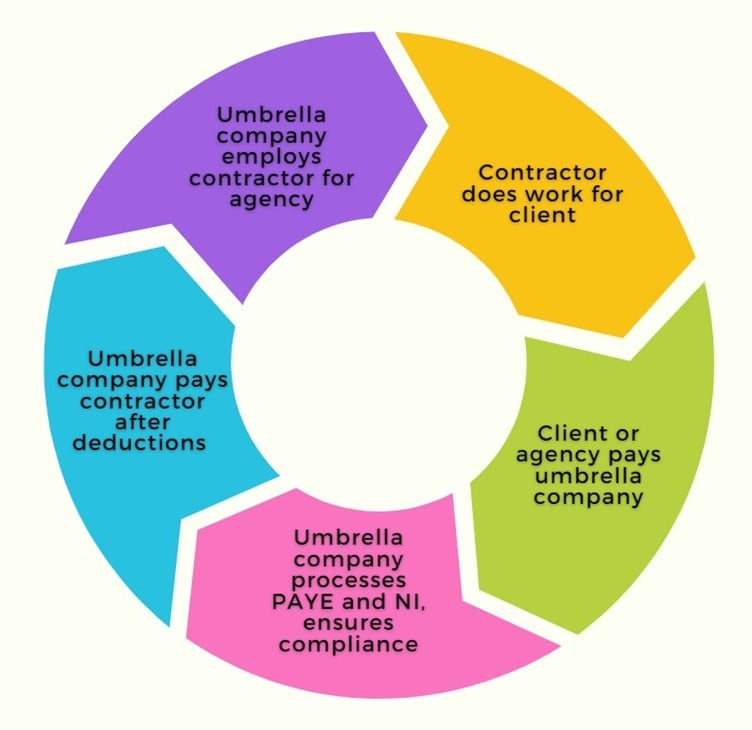

An umbrella company’s main function is to manage PAYE (Pay as You Earn) payroll on behalf of contractors. It places itself between the contractor and the client or agency and directly employs the contractor. The umbrella company receives the contractual pay from the agency, processes PAYE and National Insurance and passes on the net income to the contractor. It also takes a weekly fee or ‘margin’ – its payment for what is essentially an outsourced payroll service.

A principal reason for the existence of umbrella companies is that recruitment agencies prefer issuing contracts to limited companies. This is because when employing temporary workers directly, the agency can find itself open to a range of legal liabilities including damages stemming from the workers’ misconduct.

The basic functions of a reputable umbrella company

The umbrella company route

This arrangement offers contractors the security and convenience of being an employee. They do not need to worry about IR35 compliance (see below) as they would if operating via their own limited company. They do not have to complete the tax returns and accounts filings of a limited company. All they need to do is do the work, hand in their time sheet and the umbrella company takes care of the rest.

As an employee of the umbrella company the contractor gets the standard range of employment rights: holiday pay, statutory sick pay, protection against unfair dismissal and the other benefits of employee status. Some of these require a minimum length of continuous employment before becoming available, but even the most temporary of workers are still covered by basic employee rights. Employers are obliged to enrol their workers in a workplace pension scheme after 12 weeks of employment.

This convenience comes at a price. Income tax is standardised and removed at source, which denies the contractor opportunities to pay less tax. They must also pay the umbrella company a weekly or monthly fee for its services. This can be a fixed amount of around £100 a month or a percentage of income, typically 5%. This is significant for any level of income, but higher earners will be hit harder.

Some umbrella companies have employed murky practices that leave contractors and agencies out of pocket – see ‘mini umbrella company fraud’ below. For this reason, a prudent contractor will need to spend time checking an umbrella company’s credentials, history and trustworthiness before entering into a contract with it.

The private limited company route

Many contractors operate via their own private limited companies. This can bring tax advantages because the company director/shareholder has flexibility in how they extract profits from the limited company. They can use this flexibility to pay less tax than the fixed amount payable via PAYE as a direct employee. This is often achieved by opting to receive the most tax-efficient mix of salary and dividends. Another benefit is the absence of employee and employer National Insurance contributions.

The private limited company can pay pension contributions rather than the individual paying them out of taxed income. These contributions are often a tax-deductible expense. So pension saving can be more tax-efficient in a limited company than when working for an umbrella company. Directors of one-person limited companies also enjoy certain allowances and tax-deductible costs which, depending on circumstances, may make the limited company route more attractive.

Having a limited company allows the contractor more flexibility in work contracts. They can, to some extent at least, set out their own terms rather than merely choose whether or not to sign a ‘take it or leave it’ contract via an umbrella company.

Some clients prefer to deal with limited companies because incorporation confers a sense of security and permanence. It can be reassuring to deal with a limited company because it implies a commitment to responsibility and effective business management. It is sometimes possible to command somewhat better fees based on this preference. Agencies, as labour brokers, can sometimes find themselves involved in a race to the bottom in terms of what they charge the client and consequently what they can pass on to the contractor.

A limited company offers an opportunity to build up long-term capital. The company can be sold for cash at some point in the future, while a salaried employee of an umbrella company will have no such asset when their employment ends.

IR35, private limited companies and umbrella companies

Since the late nineties HMRC has taken arms against what it claims is tax avoidance via ‘personal service companies’ – private limited companies set up by freelancers to issue invoices, take payments and pay themselves, as described above. In this section we examine how this has affected contractors and freelancers.

HMRC has taken measures designed to make contractors with personal service companies pay broadly the same Income Tax and National Insurance contributions as individuals who are directly employed. It portrays them as employees in all but name who are ‘avoiding’ tax by ‘disguising’ themselves as contracting companies.

HMRC’s bogeyman in this regard is what it calls the ‘Friday to Monday’ worker. This is someone who quits their salaried job on a Friday and reappears on Monday to do the same work, but as a contractor. They now pay themselves a mix of salary and dividends from their own one-person limited company. In this way they ‘avoid’ paying the tax they ‘should’ be paying via PAYE as a direct employee.

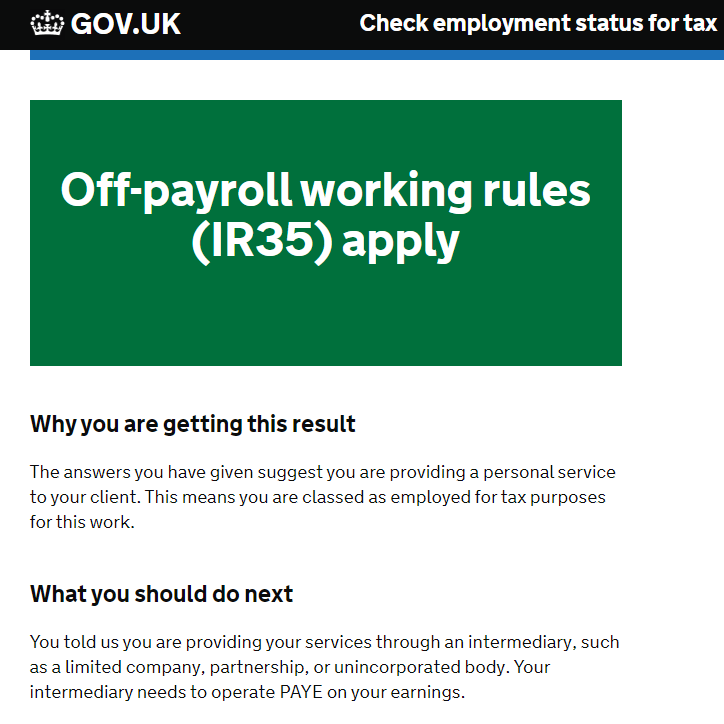

The Intermediaries Legislation (IR35) was introduced in 2000 to combat this ‘tax dodge’. It gave HMRC powers to investigate the details of contractual working relationships and decide whether to deem the client or agency the ‘employer’.

If it does, the contractor is said to be ‘inside IR35’ and taxed at source on their income. If deemed ‘outside IR35’ they are judged to be a genuine contractor and may pay their own tax. In theory at least, this unmasked the nefarious Friday to Monday worker – an employee by any other name.

Eventually HMRC became convinced that IR35 was not having the desired effect, so in 2021 it declared an amnesty. It would not open an investigation into a private company’s earlier tax compliance if the company adopted PAYE for future work.

In many cases the contractor now has no choice in the matter because new rules pass the decision about employment status to the client (if they are medium or large organisations). Deemed employers must decide whether a contractor is inside or outside IR35. HMRC police this by conducting checks on deemed employers.

Paying yourself from your private company can result in more take-home pay than umbrella working. It can still be a better option for the tax-savvy private company director. Each contractor should balance the tax breaks available to them via a limited company against the admin-free existence that comes with working for an umbrella company.

When you do form a limited company, Inform Direct takes the pain out of Companies House filing.

Mini umbrella company fraud

Criminals are known to set up multiple umbrella limited companies and constantly move workers between them to obfuscate the contractual chain and avoid paying taxes. These criminal activities have become known as mini umbrella company fraud and are a threat to workers, agencies and taxpayers. All parties should be vigilant and complete regular due diligence checks. For a list of warning signs of fraudulent umbrella company activity, see the government’s advice on mini umbrella company fraud.

Umbrella company tax avoidance schemes

HMRC publishes a list of named tax avoidance schemes operating as umbrella companies.

Inform Direct helps you keep up to date company records and make accurate and on-time Companies House filings.